Gold: Monetary Asset, Real Rates and Confidence Regimes

Gold is not a conventional commodity but a latent monetary asset. Its price tracks real rates and monetary credibility more than headline inflation, with central bank flows now reshaping the market.

Gold is not a commodity like the others. Unlike oil or copper, it is almost never consumed: it accumulates. The data behind it is compiled in our study on the impact of rate hikes on financial markets. This particularity transforms its price logic. Gold reacts less to industrial balances than to global monetary and financial regimes.

TL;DR

Over 90% of all gold ever mined is still held, so annual output (1.5–2% of the stock) barely moves the price — which instead tracks real rates and monetary credibility. More on this: Our breakdown of the FX side of international monetary regimes.

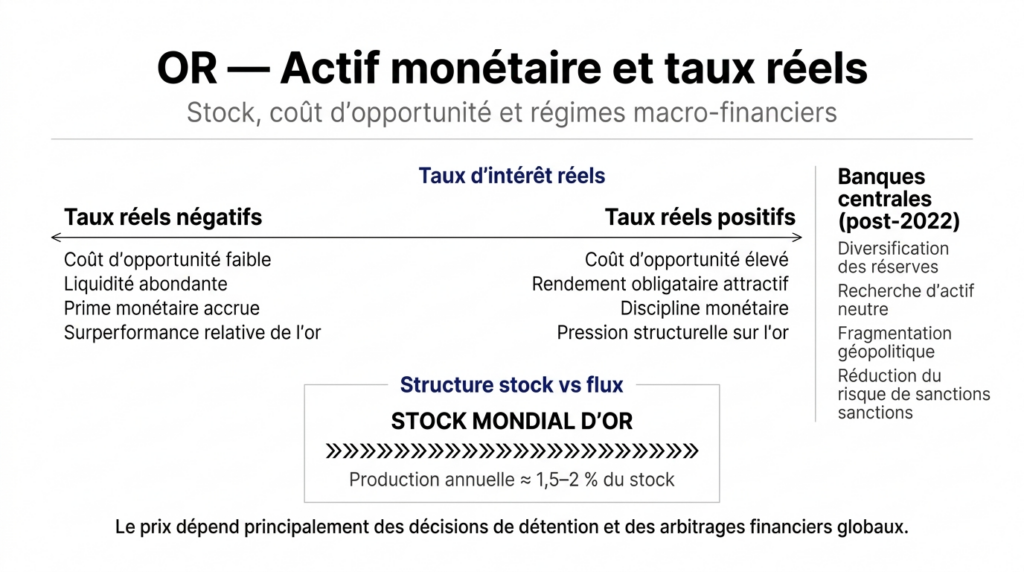

- Gold correlates with real rates, not headline inflation: when inflation-adjusted bond yields fall, the opportunity cost of holding a non-yielding asset drops; durably positive real rates exert structural pressure.

- Since 2022, net central-bank gold buying has reached historically high levels, driven by reserve diversification across several emerging economies — read as a search for a neutral asset amid geopolitical tension, not the end of the dollar.

- Gold has historically outperformed in three regimes — fast-falling real rates, lost confidence in sovereign debt, and major systemic crises — while fading when growth is stable and real rates durably positive.

Understanding gold is not analyzing a conventional commodity: it is decoding a latent monetary asset whose price depends mainly on real rates, confidence in the currency, and global financial arbitrage.

In brief:

- Gold does not mechanically track inflation: it reacts above all to real rates and monetary credibility.

- The global gold stock is enormous: annual production has little influence on price.

- Since 2022, purchases by emerging-market central banks have reshaped the structure of the market.

- Gold acts less as a short-term inflation hedge than as a monetary-regime asset.

- Its dynamic depends on global financial arbitrage and geopolitical tensions.

Gold: an anomaly in the commodity universe

Unlike copper, oil or wheat, gold is not primarily intended for consumption. More than 90% of the gold ever extracted is still held in the form of reserves, jewelry or investment bullion. Background: The decomposition of gold demand by end destination.

This fundamental feature changes everything: the gold price does not depend on a conventional industrial supply/demand balance, but on a global arbitrage between monetary holdings, financial assets and systemic confidence. That monetary-confidence arbitrage, not an industrial balance, underpins our side-by-side reading of the two decades by the cost of capital.

To place gold within its broader analytical frame, it should be situated within the logic developed in our pillar on

commodities and the global economy.

Gold appears there as a structuring exception: a physical resource whose function is above all monetary.

Gold tracks real rates, not headline inflation

The most frequent error consists in treating gold as a simple hedge against inflation. Eco3min lays this out in this dedicated note on gold monetary hedge inflation. Empirically, the most robust correlation is not with nominal inflation, but with real rates.

When real rates fall — that is, when bond yields adjusted for inflation decline — the opportunity cost of holding a non-yielding asset such as gold decreases. Conversely, durably positive real rates exert structural pressure. For context: The long-run real gold trajectory.

Gold is therefore not a barometer of consumer prices, but an indicator of monetary credibility.

Stock vs flow: why mining supply is secondary

Annual gold production represents about 1.5 to 2% of the existing global stock. This proportion is marginal compared with other commodities.

For oil or copper, a 2–3% deficit can trigger an immediate price shock. For gold, the effect is far more diffuse. The market is dominated by holding decisions of investors, funds and central banks.

The formation of the gold price perfectly illustrates the mechanisms described in our sub-pillar on the

formation of commodity prices:

price is not driven solely by physical quantities but by expectations, liquidity and global financial arbitrage.

Central banks: the return of a structural actor

Since 2022, net gold purchases by central banks have reached historically high levels. The phenomenon reflects a gradual diversification of reserves, particularly across several emerging economies.

This move should not be read as the “end of the dollar,” but as a search for a neutral asset in a period of geopolitical tensions.

This dimension connects directly to the dynamics analyzed in our sub-pillar on the

geoeconomics of resources:

gold becomes an instrument of strategic autonomy more than a simple financial asset.

Gold as a regime asset

Historically, gold has outperformed in three configurations:

- rapid erosion of real rates;

- loss of confidence in sovereign debt;

- major systemic crises.

By contrast, in regimes of stable growth and durably positive real rates, its relative performance tends to fade.

Gold is therefore neither a conventional cyclical asset nor a purely defensive one. It is a transition asset between monetary regimes.

Gold, the dollar and geopolitical fragmentation

The inverse relationship between gold and the dollar remains dominant, but it is not mechanical. During phases of global stress, both can rise simultaneously: the dollar as safe-haven liquidity, gold as an asset outside the banking system. Our study of the financial performance hierarchy under a strong dollar traces this relationship across decades.

In a world marked by geopolitical fragmentation, the question is no longer purely monetary, but strategic: which assets remain neutral in the event of sanctions, asset freezes or trade tensions?

Gold retains a unique function here.

Analytical implications for investors

Gold should not be treated as a conventional industrial commodity. Its role within a portfolio relates more to:

- regime diversification;

- a hedge against monetary-policy errors;

- protection against extreme systemic shocks.

By contrast, it offers neither intrinsic yield nor automatic protection across all inflationary phases.

Conclusion: gold, silent mirror of the monetary system

Gold is neither an anecdotal speculative asset nor a relic of the past. It is a leading indicator of monetary and geopolitical tensions.

In a world where the cost of capital is once again structuring and where public debt has reached historically high levels, gold functions as a marker of systemic credibility.

It does not predict crises, but it signals deep imbalances before they become visible in conventional macroeconomic indicators. This finding is grounded in the data in our study of the silent imbalances a strong dollar builds.

3 takeaways

- Gold tracks real rates more than inflation.

- Its price depends more on holding decisions than on mining output.

- It acts as a regime asset in an uncertain monetary environment.

Last updated — 12 July 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

Full pillar →Euro Below Parity in 2022: What Parity Means

In September 2022, the euro fell below parity with the dollar, to around 0.95, a low not seen…

Eurozone Fragmentation: Sovereign Spreads and the Euro

The euro is issued by a monetary union without a complete fiscal union: nineteen sovereign debts coexist under…

The Euro’s Energy Import Bill: the Gas Shock and the Currency

In 2022, the surge in gas prices turned the euro area's historic current-account surplus into a deficit and…