Why Rental Yield Often Overstates Actual Property Returns

Gross cash flows, hidden costs and time horizons explain why rental yield frequently overstates the real economic performance of residential property investments.

Rental yield offers a partial reading of property profitability, because it ignores the role of credit, real charges and adjustments over time.

TL;DR

Rental yield freezes one ratio, rent over price, while credit costs, charges and vacancy keep moving, so an attractive headline yield can mask eroding net returns once financing is included.

- Rental yield assumes stable financing, but as euro-area mortgage rates rose from around 1.5% to nearly 4% between 2022 and 2024, the financial burden grew faster than rents collected while headline yield stayed unchanged.

- Over 2019-2025, condominium charges, maintenance and some local taxes rose faster than rents in many tight markets, with rental vacancy adding a disproportionate hit to annual profitability.

- The financial effort ratio, the path of non-recoverable charges and average vacancy duration track effective profitability more faithfully than the rents-to-price ratio alone.

A widely held view reduces property profitability to a simple percentage: gross or net rental yield. This reading is intuitive, fast, and widely used in property comparisons. Yet it frequently produces a distorted perception of actual performance, especially in an environment of durably higher rates. Yield captures neither the financial structure of the operation nor the frictions that emerge over time. (same vein: the overstatement of returns baked into gross yield). A broader view: the Eco3min framework on how credit and volumes drive property prices.

This gap has become more visible since the tightening of credit conditions observed between 2022 and 2025, where rising monthly payments and contracting volumes have altered the economic balance of property investments without always immediately affecting listed rents.

Rental yield: a static indicator facing a financial dynamic

Rental yield rests on a simple ratio: annual rents divided by property price. This approach implicitly assumes stable financing conditions and charges. In practice, however, real estate is an asset heavily dependent on credit. When mortgage rates in the euro area rose from around 1.5% to nearly 4% between 2022 and 2024, the annual financial burden increased far faster than the rents collected. This transmission mechanism is documented in our reading of the property credit cycle and its lag on prices.

Headline yield then remains unchanged, while net profitability deteriorates. This dissociation explains why properties may appear attractive on paper while delivering economic performance below expectations once financial, fiscal and operational charges are factored in.

This gap reflects the fact that rising rates first act through the credit channel before affecting rents or prices, a mechanism analyzed in detail in the study on the transmission of rates to property prices.

The underestimated role of credit in effective profitability

Part of the consensus assumes that rental yield is enough to compare two property investments. This assumption holds in an environment of low and stable rates, where credit plays a secondary role. Once financing turns into the central variable, gross yield gives way to net-net rental profitability read against the cost of capital. It becomes fragile when financing becomes the central adjustment variable.

In a context of bank tightening, profitability depends more on the structure of credit than on the level of rent. The mechanism is similar to that described in the analysis of counterintuitive reactions in the property market: adjustment first comes through financing capacity, not through prices or rents.

In other words, two properties displaying the same rental yield can produce very different financial trajectories depending on credit duration, effective rate and refinancing conditions.

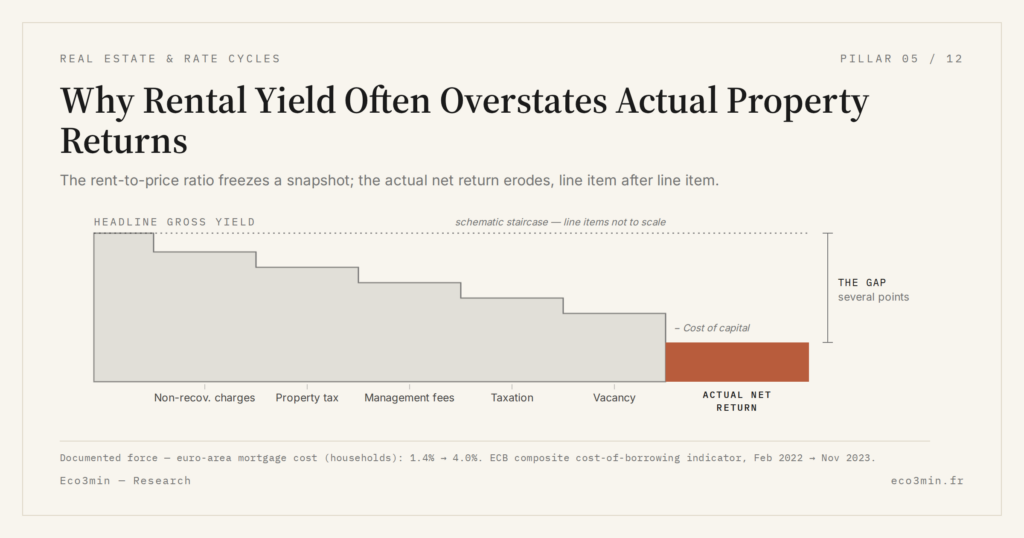

Real charges, vacancy and invisible frictions

Rental yield is often calculated excluding frictions. Yet over the 2019–2025 period, condominium charges, maintenance costs and certain local taxes rose faster than rents in many tight markets. Reading the REIT dividend beyond yield draws out the consequences for listed property. To this are added periods of rental vacancy which, even if short, have a disproportionate effect on annual profitability.

These elements do not call into question the economic interest of real estate, but they highlight the limit of an indicator that freezes a reality which is in fact moving. Actual profitability is built over time, through an accumulation of costs and adjustments that yield does not capture. Related framing: the trade-offs across real-estate routes.

This static reading also explains why real estate may be perceived as a hedge against inflation while real cash flows are weakening — a point developed in the analysis on the limits of property as inflation protection.

What many are really trying to understand

Behind the question of yield, the real interrogation concerns the robustness of the trajectory: does a property remain profitable when financing conditions change? Yield answers an instantaneous snapshot, not the resilience of the economic model in the face of cycles in rates, credit and taxation. A parallel read: Our REITs-versus-physical real estate comparison.

This distinction joins the broader reading proposed by the pillar page on property cycles and rates, which shows why static indicators struggle to reflect actual dynamics.

Counter-arguments and limits of this reading

In an environment of durably low rates and strong rental tension, yield can remain a relevant short-term indicator. Likewise, certain very specific segments — characterized by indexed rents or low vacancy — better absorb financial shocks. These situations are not, however, the central scenario observed since 2024.

If credit conditions were to ease quickly or if rents were to adjust strongly upward, the divergence between headline yield and actual profitability could narrow.

Observable economic implications

For households, this overstatement of yield complicates the assessment of actual housing cost over time. For firms in the sector, it contributes to maintaining asset prices disconnected from their economic performance. At the macroeconomic level, it blurs the reading of monetary transmission, by masking the effect of credit behind apparently stable ratios. The broader treatment appears in the split between collective property vehicles and direct letting.

Equating high rental yield with robust profitability, without integrating credit costs, real charges and the time-related frictions that shift the economic trajectory.

Indicators to track for reading the actual gap

More than headline yield, certain indicators provide a better appreciation of effective profitability: the financial effort ratio, the evolution of non-recoverable charges and the average vacancy duration. Their combination offers a more faithful reading of economic performance than the rents-to-price ratio alone.

- Rental yield measures a snapshot, not a complete financial trajectory.

- Credit costs and charges explain much of the gap between headline yield and actual profitability.

- In a high-rate context, the static reading becomes particularly misleading.

The overstatement of rental yield does not reflect a one-off anomaly but a structural limit of the indicator. It is a reminder that, in real estate as in other asset classes, performance never reduces to a single ratio.

Last updated — 21 July 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

Full pillar →US Rental Property Real Yield: What Cap Rate and NOI Actually Leave You

A rental listing leads with a yield. Divide the annual rent by the price and the number looks…

Cap Rate Spread: What Rental Yield Pays Over the 10-Year Treasury

A 5% cap rate sounds attractive. But 5% against what? A risk-free 10-year Treasury yields near 4.5% in…

US Rental NOI, Line by Line: What Net Operating Income Really Subtracts

A US rental yield is advertised gross: annual rent over price. Between that number and the income an…