Bitcoin: why its volatility is falling (2011-2026)

Bitcoin’s volatility has compressed from the 2011 extremes toward a durably calmer regime — a gradual maturation that regulation accompanies, without having caused it.

TL;DR

Bitcoin's calmer regime traces to a decade of market maturation (deeper liquidity, larger capitalization) that MiCA and the 2024 spot ETFs formalized rather than caused.

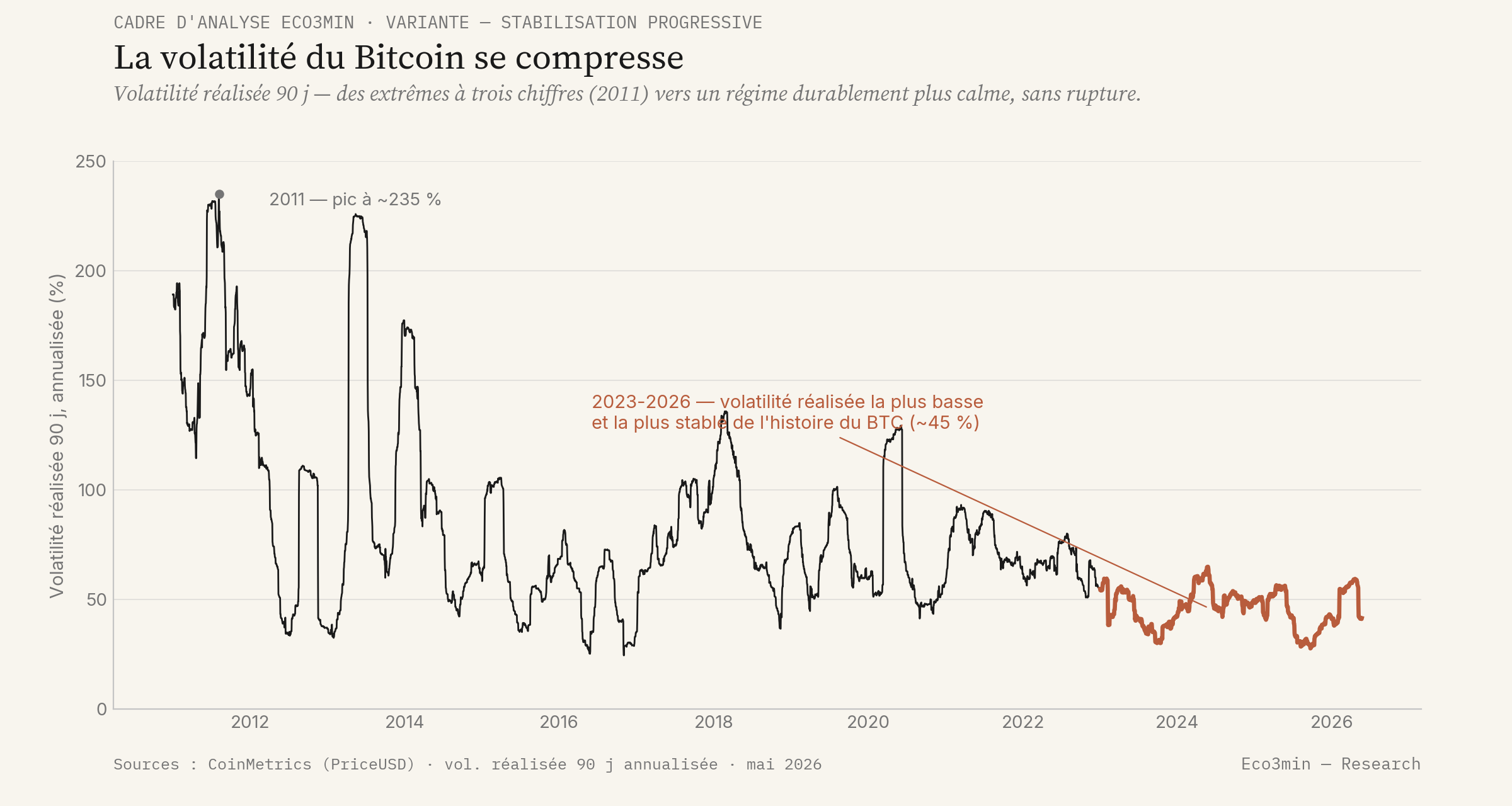

- Realized volatility (90-day, annualized) fell from a roughly 235% peak in 2011 to about 45% over 2023-2026, its lowest and steadiest level, but not in a straight line: a 70-80% plateau held over 2014-2021 and 2026 rebounded above the recent step (CoinMetrics).

- The chronology weighs against a regulatory cause: most of the lower step settled over 2022-2023, before MiCA entered application, and the decline runs back more than a decade. Regulation recorded the calm; it did not create it.

- Lower volatility measures more contained swings, not safety: counterparty and fraud risk, including the 2022 crypto collapses, sit outside this metric, and those collapses were absorbed without spreading to the traditional financial system.

Some asset classes stabilize without any triggering crisis marking the turn. Fragility does not vanish at once: it recedes gradually, as the market deepens and the most fragile actors are filtered out. This is the variant of the fourth silent adjustment regime Eco3min documents: a diffuse stabilization that regulation formalizes rather than triggers.

Bitcoin provides a measurable case. Its realized volatility has fallen several-fold between its early days and today. The temptation is to attribute this calm to the entry into force of the European MiCA regulation (2024) — but the data demands caution: the compression began well before, it is neither linear nor secured. The useful question is therefore not “did regulation stabilize Bitcoin?”, but “how to read a gradual stabilization that regulation accompanies without being its cause?”.

The observable fact — the compression of volatility

Bitcoin’s realized volatility (measured over 90 days, annualized) falls from a peak of about 235% in 2011 to a regime of about 45% over 2023-2026 — the lowest and most stable of its history. The trajectory is not a downward straight line, though: after the extremes of the early years, it settles on a plateau on the order of 70-80% between 2014 and 2021, before stepping down to a markedly lower level from 2022-2023. And the decline is not definitive: 2026 rebounds above the average of the recent step. The underlying price series is tracked in the dataset Bitcoin price history.

Realized volatility measures the average amplitude of past price moves — nothing else. Lower volatility means more contained swings, not the absence of risk: counterparty risk, fraud, or the failure of an actor (the 2022 collapses) remain entirely in place and do not show up in this measure. Confusing “less volatile” with “safer” is the most common interpretation error on crypto-assets. The evidence is gathered in our analysis of crypto regulation.

The mechanism: a maturation, not a decree

The compression of volatility is explained first by market factors: deepening liquidity, a broadening base of participants, the development of derivatives markets, and above all the growth of capitalization — the larger an asset, the smaller a given move represents as a percentage. The arrival of regulated vehicles (the spot ETFs approved in early 2024) also integrates Bitcoin into supervised channels. That move into supervised channels runs parallel to the US stablecoin regulatory framework taking shape on the dollar-token side.

Regulation — MiCA in Europe, the framing of stablecoins — intervenes in this movement as a formalization of the filtering of the most fragile actors, not as its origin. The chronology imposes this: most of the low step settles over 2022-2023, before MiCA enters into application, and the long-term decline goes back more than a decade. Reading regulation as the cause of stability would be to confuse concomitance with causality — the classic trap of misleading indicators.

A stabilization without a triggering crisis

The distinctive trait of the regime is the absence of a visible tipping point. Crypto-assets went through violent internal collapses in 2022 (actors and protocols), but these did not trigger contagion to the traditional financial system — they were absorbed, and the filtering of actors continued without systemic rupture. No single episode marks the passage to a calmer regime: the stabilization is diffuse, spread out, and regulation comes to record its state rather than force its course. This is exactly the logic of crypto-assets in a maturation phase.

What the case reveals about how markets work

A gradual maturation can take on the appearance of a piloted stabilization. Regulation, arriving after the fact, optically inherits a calm it did not create. For an observer, the difficulty is to distinguish what stems from a structural market dynamic from what stems from an intervention — and to resist the comfortable narrative causality. This reading belongs to the grid of the pillar page financial markets and complements the other regimes with the cases of the yen and Volmageddon.

An asset class can stabilize without a triggering crisis, through gradual filtering of fragile actors. The regulation that comes afterward formalizes this state — attributing it as cause confuses the chronology with the mechanism.

Scope, limits and condition of invalidation

This is the most cautious case of the series, and its limits must be explicit. The compression of volatility is real but not monotonic (2014-2021 plateau), incomplete and reversible (2026 rebound, spikes still possible), and the fall in volatility says nothing about counterparty or fraud risk. Above all, the link with regulation is concomitant, not causal: the chronology forbids it. The regime would be invalidated if realized volatility durably climbed back toward triple-digit levels, or if a crypto shock this time propagated to the traditional financial system — a sign that the supposed filtering had not worked. Our study on the structural drivers behind crypto volatility sheds light on this aspect.

The stabilization of an asset can be a market maturation that regulation accompanies, without having caused it. Falling volatility measures more contained swings — not the disappearance of risk, nor the effect of a decree.

- Bitcoin’s realized volatility falls from a ~235% peak (2011) to a ~45% regime (2023-2026), the lowest and most stable of its history.

- The decline is real but not monotonic (2014-2021 plateau) and incomplete (2026 rebound): nothing is secured.

- Regulation (MiCA 2024, spot ETFs) is concomitant, not causal: most of the low step precedes MiCA.

- Lower volatility ≠ lower risk: counterparty and fraud stay outside this measure.

Data and further reading

Overall framework: the silent adjustment regimes (variant). Related cases: the yen, Volmageddon. Data series: Bitcoin price history. Pillar: crypto-assets. All proprietary macro-financial data (CSV/XLSX): Data & research hub.

Last updated — 21 July 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

Full pillar →Bitcoin Halving: How the Programmed Supply Cut Works

The halving writes bitcoin’s scarcity into an immutable rule, applied without exception since 2012. It shapes the pace…

Crypto Cycles: Why Their Amplitude Dwarfs Equity Swings

Crypto cycles post drawdowns two to four times deeper than equity markets. The asymmetry stems from market microstructure,…

Bitcoin Cycle: A Quiet Inflection the Market Is Still Ignoring

A quiet on-chain indicator points to a different Bitcoin market regime, with material implications for allocation framing and…