DGS10 and Treasury Demand: Fiscal Deficit, Issuance and Bond Market Stress

Record Treasury issuance since 2022 and the recomposition of the buyer base durably structure the DGS10 term premium. Understanding this supply-demand equation has become a prerequisite for reading the 10-year yield in the contemporary fiscal regime.

TL;DR

Record post-2022 Treasury supply meets a buyer base now dominated by price-sensitive holders, and that shift alone rebuilds the term premium that decouples DGS10 from Fed Funds expectations.

- An October 2024 Hudson Bay Capital paper by Stephen Miran, later Council of Economic Advisers chair, argued the Treasury's heavier Bills tilt in 2022-2024 amounted to unannounced stealth easing, turning issuance composition into a policy variable alongside the Fed Funds path.

- Because the Fed runs down its balance sheet while the Treasury keeps issuing, the private market absorbs new supply and Fed roll-offs at once; this double pressure, visible in autumn 2023 and late 2024, rebuilt the term premium even as Fed Funds expectations softened.

DGS10 does not form in a monetary isolation chamber: it incorporates a fiscal component that joined the pricing in 2022 and has not left the table since.

1. The U.S. fiscal trajectory 2022-2026

The U.S. federal deficit oscillated around 6.5% of GDP over 2023-2025, an unusual configuration outside recession or war periods. The Congressional Budget Office (CBO), in its August 2024 projections, anticipates an average deficit of 6.1% of GDP over the 2025-2034 decade, with publicly held debt moving from 99% of GDP at end-2024 to 122% by 2034. This trajectory is unprecedented in peacetime in modern U.S. history. The related interest burden is tracked in the history of the federal interest burden relative to GDP.

The operational consequence is the explosion of Treasury issuance. The Treasury Department issued approximately $3.5 trillion net in fiscal year 2024, against $1.8 trillion in 2019. The issuance composition has also shifted: the share of Bills (maturity ≤ 1 year) in new issuance temporarily reached 80% in 2023 before falling back toward 25-30% in 2024-2025, mechanically transferring more pressure to the Coupons segment (2 to 30 years) where DGS10 forms. This pressure on Coupons supply is one of the structuring channels shaping the central macro role of DGS10 in the current cycle.

The Treasury Borrowing Advisory Committee (TBAC) publishes quarterly recommendations on issuance composition. The 2024-2025 TBAC reports warn about the capacity of the buyer base to absorb anticipated volumes, particularly on the 7-30 year maturities where structural demand has eroded since the QE exit. A related angle is set out in the map of bond ETFs by rate sensitivity.

2. The recomposition of the Treasury buyer base

The Treasury International Capital (TIC) data published by the Treasury Department allow tracing the evolution of buyer cohorts since the 1970s. Four main cohorts structure demand: foreign official holders (central banks, sovereign funds), private foreign holders, the Federal Reserve itself, and domestic holders (banks, pension funds, mutual funds, households).

The composition has evolved in structuring ways. The share of foreign official holders went from approximately 40% of outstanding Treasury debt in 2014 to 22-24% by end-2025. This percentage decline masks near-stagnation in absolute terms (around $3.5-3.8 trillion), but means that at the margin, rate-sensitive private buyers absorb new issuance. The Fed, which held 25% of Treasury debt in 2022 at the COVID QE peak, reduced this share to about 16% by end-2025 via quantitative tightening (balance sheet reduction of about $2 trillion since mid-2022).

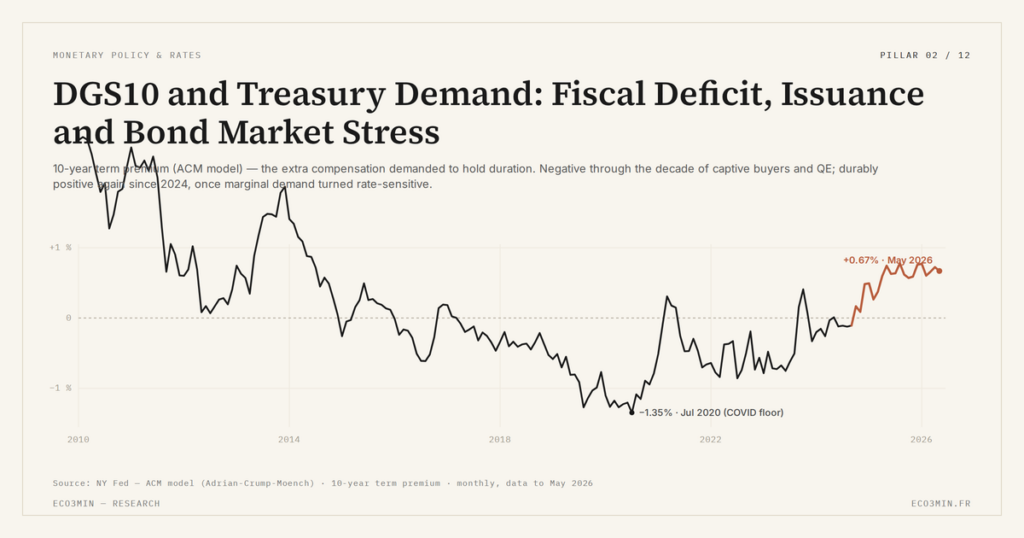

The aggregate result is a deep recomposition of marginal demand. In 2014, the Treasury market was dominated by price-insensitive buyers (foreign central banks in accumulation, Fed in QE). In 2025-2026, it is dominated by price-sensitive buyers: pension funds adjusting duration based on yield, hedge funds exploiting basis arbitrages, asset managers tracking their benchmark. This transition partly explains the return of the term premium to positive territory after a negative decade — a phenomenon analyzed via the role of the ACM term premium in the transmission mechanism.

3. How the supply-demand equation transmits to DGS10

Standard financial theory assumes Treasuries are “near-money” — securities of such liquidity and credit quality that their price essentially reflects expected Fed Funds plus a quasi-stable term premium. This assumption was largely valid over 2010-2021 thanks to the combination of captive buyers and structural QE. It is now being challenged. The data behind this: our 10-year term-premium series.

Three channels describe how the supply-demand equation now weighs on DGS10. First channel: the ACM term premium published by the NY Fed incorporates the premium demanded by marginal holders to bear duration risk. When marginal demand becomes more rate-sensitive, this premium mechanically rebuilds. The +60 bps observed at end-2023 and the +30 to +40 bps in 2025-2026 are the materialization of this channel. This is precisely the component that the accounting identity DGS10 = TIPS + breakeven does not explicitly capture, hidden inside the nominal leg.

Second channel: auction tails. When the allocation yield of a Treasury auction exceeds the pre-auction indicative yield, it signals that primary demand is insufficient at the anticipated price. The 10-year and 30-year auctions of summer 2023 and autumn 2024 produced 2-5 bps tails, a modest but unusual level compared with the previous decade. These primary signals then transmit to the secondary yield within days. Common misreadings of these signals are addressed in the most common misreadings of bonds and interest rates.

Third channel: repo financing conditions. When Treasury issuance pressure saturates primary dealer balance sheets, the cost of financing their positions rises via repo. This cost transmits to yields through widened bid-ask spreads and reduced liquidity in the secondary market. The MOVE Index (Treasury option implied volatility) partially captures this dynamic: its 2023 and 2024 peaks coincided with pressure phases on the primary dealers / repo chain.

A worthwhile structural element is the policy debate around the Treasury’s choice between Bills and Coupons in funding the deficit. The Hudson Bay Capital paper of October 2024 by Stephen Miran (later Council of Economic Advisers chair) explicitly criticized the 2022-2024 Treasury choice to fund deficits with a higher share of Bills than coupon-issuance ratios would have implied, arguing this represented an unannounced form of stealth easing. The debate is empirically open — some analysts contest the magnitude of the effect — but it documents how the issuance composition itself becomes a policy variable that interacts with the Fed Funds path. Going forward, the normalization of Bills versus Coupons share remains a key swing variable for DGS10 dynamics. A related fiscal angle is developed in Gold as a counterpart to U.S. fiscal deterioration.

4. Indicators of Treasury demand stress

Four indicators allow real-time monitoring of Treasury demand health. First indicator: auction bid-to-cover ratios, published by the Treasury immediately after each issuance. These ratios measure total amount bid divided by amount allotted. A stable bid-to-cover at 2.3-2.5x on 10-year auctions signals healthy demand; a durable decline below 2.2x would signal stress.

Second indicator: allocation breakdown by cohort (indirect bidders, primary dealers, direct bidders). Indirect bidders are approximately foreign central banks and international institutions. Their allotted share oscillated between 65 and 75% over 2018-2023; a persistent decline below 60% would signal foreign withdrawal from primary demand and shift the burden to primary dealers, who eventually resell in the secondary market at higher yields.

Third indicator: the ACM term premium decomposition. A term premium expansion beyond +75 bps would signal that holders demand structurally higher compensation for bearing duration — revealing a regime change in the perception of Treasury as a safe asset. This dynamic is articulated with the historical reading provided by the DGS10 regime opened since 2022.

Fourth indicator: 5-year sovereign CDS on the U.S., which measure the credit risk premium demanded to insure Treasury exposure. These CDS oscillated below 30 bps over 2014-2021, jumped to 165 bps in May 2023 during the debt ceiling debate, then fell back to 40-50 bps after the political agreement. A structural rise above 80 bps would signal durable integration of sovereign risk in Treasury pricing.

The interaction between Treasury issuance pressure and Fed quantitative tightening creates a particular dynamic. When the Fed runs off its balance sheet via QT, it effectively requires the private market to absorb both new Treasury issuance and Fed roll-offs. This double pressure was visible in autumn 2023 and again in late 2024, and is one of the structural reasons why the term premium rebuilt despite Fed Funds expectations softening. The QT pace announced by the FOMC therefore constitutes a complementary tightening lever to Fed Funds itself, with a transmission to DGS10 that differs from the policy rate channel. A companion piece: the channel from policy rates to company results.

5. Frontier with other sensitive markets

DGS10 forms a natural frontier with several other markets whose dynamics depend on its reading. High Yield Option-Adjusted Spreads (HY OAS) follow a complex correlation with DGS10: in risk-on regime, they can compress even when DGS10 rises (yield search); in risk-off regime, they widen independently of DGS10 (flight to quality). This context also illuminates the analytical significance of the 4% threshold, part of which stems precisely from the structural issuance pressure described here. The articulation between these two variables depends on the DGS10 driver — if the yield rises through fiscal term premium, HY OAS widens; if it rises through growth anticipation, they may remain stable.

The short-term money market forms another frontier. The monetary transmission of policy rates via DGS10 to corporate financing conditions depends on the prior functioning of the Treasury primary market. When it absorbs new issuance correctly, financial conditions remain fluid; when it saturates (2023, 2024 episodes on some segments), financial conditions tighten beyond what Fed Funds anticipate. Because interest payments alone drive part of that issuance, the share they represent is isolated by the primary-balance reading of public finances.

Another frontier, more recent, is that of dollar-denominated stablecoins. Stablecoin issuers (USDC, USDT) became significant net Treasury Bill buyers since 2023, and their growth could partially redraw short-term demand composition. This dynamic nevertheless remains concentrated on Bills (≤ 1 year) and does not directly affect DGS10 formation, which sits on Coupons.

- The U.S. federal deficit around 6.5% of GDP and debt at 120% of GDP durably structure Treasury issuance pressure, particularly on Coupons where DGS10 forms.

- The recomposition of the buyer base (foreign official share from 40% in 2014 to 22-24% end-2025, Fed from 25% to 16%) shifts marginal demand toward rate-sensitive buyers, mechanically rebuilding the term premium.

- The ACM term premium published by the NY Fed, back in positive territory since 2022 (+60 bps end-2023, +30 to +40 bps in 2025-2026), captures this supply-demand dynamic and explains a substantial share of decoupling phases between DGS10 and expected Fed Funds.

- Monitoring Treasury demand goes through four indicators: bid-to-cover ratios, allocation breakdown by cohort, ACM term premium level, and 5-year sovereign CDS on the U.S. — to be tracked jointly, not in isolation.

Last updated — 22 July 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

Full pillar →Real Rates: The True Cost of Capital Is Repricing

Why real rates are reasserting themselves as markets' anchor and how to recalibrate investment and financing decisions facing…

Real Interest Rates: The Quiet Signal Reshaping Markets

Real interest rates: why their persistence in positive territory in 2026 is reshaping the rules for bonds, equities,…

OAT-Bund Spread: A Quiet Gauge of French Sovereign Risk

OAT-Bund spread: how this yield gap has become a key signal on French sovereign risk, fiscal policy and…