DGS10 vs TIPS vs Breakeven: Decomposing Nominal Yields Into Real Rates and Expectations

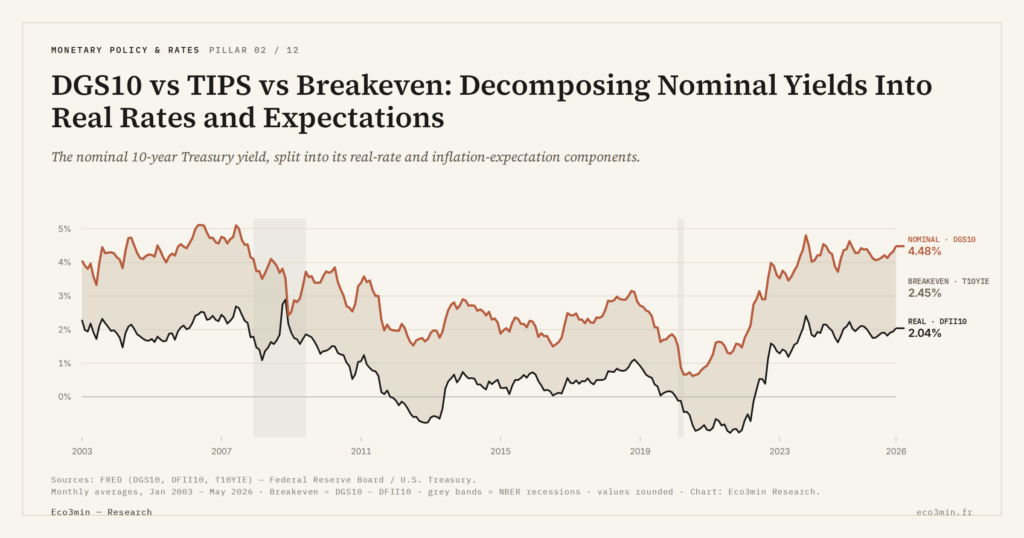

DGS10 is a composite number aggregating three distinct factors: real yield, inflation expectations, and term premium. The accounting identity DGS10 = DFII10 + T10YIE allows empirically settling between contradictory readings of the same move.

TL;DR

DGS10's decomposition reads three macro questions out of one number: 2008 priced a deflation scare, 2013 and 2023 priced real-rate repricings, 2024 hid an internal rotation behind a flat nominal.

- The Fed's daily identity DGS10 = DFII10 + T10YIE makes the breakeven a deduced, not measured, quantity (DFII10 published since January 2003); reading all three on the same date settles whether a move is real or inflation-driven.

- In late 2008 DGS10 fell from 3.9% to 2.1%, about 60% of it a breakeven collapse, with T10YIE briefly near -0.5% in November 2008 signaling 10-year deflation expectations rather than a flight to quality.

- The 2013 taper tantrum (1.66% to 2.98%) ran about 85% through the real leg and the September-October 2023 ZIRP exit (3.8% to 5.0%) about 80%, both repricing term premium and r-star rather than inflation.

- The dominant component rotates by regime: the breakeven drove roughly 60% of DGS10 variance over 1985-1995, the real leg about 65% under 2010-2021 QE, with the two roughly balanced again across 2022-2024.

Without this decomposition, a yield move remains an opaque aggregate; with it, every episode becomes readable in distinct economic components.

1. The accounting identity that structures the reading

The Federal Reserve publishes daily three series that together form an exact accounting identity: DGS10 (the nominal 10-year Treasury yield), DFII10 (the ex-ante real yield on the 10-year TIPS, available since January 2003), and T10YIE (the inflation breakeven, computed by construction as DGS10 minus DFII10, available as the FRED T10YIE breakeven series). The relationship is tautological on the calculation side: T10YIE is not directly measured but deduced. It is no less operationally decisive for interpreting a move. what TIPS hedge and what they don’t sets out the mechanism in detail.

When DGS10 rises from 3.0% to 4.5%, two opposing readings coexist in market commentary. First: “inflation expectations have reawakened.” Second: “real yields have moved up.” Both can be true, only one of them, or neither. Without looking at DFII10 and T10YIE on the same day, the commentator projects a preferred narrative onto a number that does not contain it. With the decomposition, the question becomes empirical and settled.

This identity offers a compositional reading of what the pivot role of DGS10 in U.S. macro aggregates daily into a single number. It rests on the Constant Maturity plumbing behind the published yield: DGS10 and DFII10 follow the same CMT method, making their subtraction methodologically coherent. T10YIE directly inherits the biases and smoothings of the method applied to both underlying series — a dependency to keep in mind during Treasury stress phases.

2. Reading a DGS10 move through its decomposition

The minimal discipline is to publish, alongside every DGS10 commentary, the levels of DFII10 and T10YIE on the same date. A +30 bps DGS10 move over 5 days can take three qualitatively distinct forms. First case: +30 bps real and 0 on breakeven (pure real tightening, typically associated with an upward r-star revision or a term premium repricing). Second case: +5 bps real and +25 bps breakeven (inflation expectations reawakening, a rarer configuration since 2014). Third case: +15 bps real and +15 bps breakeven (mixed move, the most frequent configuration in the 2022-2024 episodes). A related fiscal angle is developed in federal debt read as a driver of monetary metal.

The three cases have radically different economic implications. Case 1 tightens the real cost of capital without additional inflation — it mechanically weighs on equity valuations and the housing market. Case 2 preserves real returns but raises the inflation bill for cash holders and nominal bond holders. Case 3 combines both effects. The transmission channel through real yields illustrates how these decompositions propagate differently to corporate balance sheets.

The elasticity of each component to the economic cycle differs. DFII10 mainly tracks the expected r-star trajectory and the real term premium, reacting to growth and productivity surprises. T10YIE follows CPI surprises, survey-based inflation expectations (Michigan, NY Fed Survey of Consumer Expectations), and monetary policy expectations conditional on inflation. This elasticity difference makes it possible to identify which macroeconomic channel dominates in a given move — a diagnosis impossible from the nominal DGS10 alone. Related series: the term-premium data series.

Mapping the dominant component over historical samples reveals interesting patterns. Over 1985-1995, T10YIE drove roughly 60% of DGS10 variance — the disinflation regime was readable primarily through inflation expectation collapse. Over 1995-2007, the split shifted toward roughly 45% real and 55% breakeven, reflecting both productivity gains visible in DFII10 and stable inflation expectations. Over 2010-2021 under QE, the real component dominated again (around 65% of variance) as inflation expectations were anchored by Fed credibility while real yields fluctuated with QE flows. The 2022-2024 window saw a return of breakeven volatility, with shares roughly balanced between real and inflation contributions. Companion analysis: what an inflation-linked bond does and does not protect.

The same decomposition applies to reading by level, not only by variation. A 4% DGS10 can be composed of 2% real and 2% breakeven (a configuration historically consistent with cyclical equilibrium), or 0.5% real and 3.5% breakeven (an economy under inflation stress), or 3% real and 1% breakeven (an economy under real stress without inflation). This is precisely what structures how the 4% threshold decomposes into real and breakeven.

3. Three historical episodes decomposed

Three episodes document the operational usefulness of the decomposition.

October 2008, post-Lehman. DGS10 fell from 3.9% to 2.1% between September and December 2008. The decomposition shows this drop was driven roughly 60% by the breakeven collapse (T10YIE moved briefly into negative territory, around -0.5% in November 2008, signaling 10-year deflation expectations), and 40% by the DFII10 decline. This is not a classic flight-to-quality — it is a dramatic downward revision of inflation expectations. That sharp downward revision of expectations sits within how the nature of the shock steers what resists. Without the decomposition, the move could have been read as simple safe-asset rotation, masking the implicit deflation forecast.

May-August 2013, taper tantrum. DGS10 rose from 1.66% to 2.98% in four months after Bernanke mentioned a future slowdown in asset purchases. The decomposition reveals this move was driven 85% by the real leg (DFII10 from -0.75% to +0.75%, a 150 bps move) and only 15% by breakeven. It was a pure repricing of the term premium and real Fed Funds expectations, without notable inflation expectation awakening. This reading would have spared commentators of the era the confusion between anticipated monetary tightening and reflation. Related coverage: our TIPS-versus-nominal Treasuries comparison.

September-October 2023, ZIRP exit. DGS10 moved from 3.8% to 5.0% in six weeks, a brutal repricing marking the peak of the post-COVID cycle. The decomposition gives approximately 80% real leg (DFII10 from 1.5% to 2.5%, +100 bps) and 20% breakeven (T10YIE from 2.3% to 2.5%, +20 bps). This is one of the most purely real-driven moves of the decade: markets repriced r-star and the term premium, not inflation. This characterization is essential for reading the 2022-2026 regime within the historical series.

A fourth case, more recent, deserves mention: the April-June 2024 period, when DGS10 oscillated in a narrow range of 4.2% to 4.7% while the breakeven compressed from 2.55% to 2.25% and DFII10 rose from 1.65% to 2.45%. The decomposition reveals a hidden move behind the apparent nominal stability: inflation expectations normalized while real yields rose 80 bps. A commentator looking only at DGS10 would have concluded macroeconomic stability; the decomposition shows instead an internal rotation of components that durably supported pressure on equity valuations and real estate.

Each episode highlighted a different macro question: 2008 a deflation risk, 2013 a monetary transition, 2023 a regime change in real rates, 2024 a hidden internal rotation. None of these characterizations would have been possible from DGS10 alone. The discipline of systematically publishing the three-way decomposition is the most reliable safeguard against narrative projection on yield moves. The wider context: how monetary policy lands on corporate margins.

The persistence of this decomposition discipline distinguishes serious fixed income analysis from headline-driven commentary. Bloomberg Markets, the Financial Times’ Alphaville, and the NY Fed Liberty Street Economics blog all routinely publish the three-way decomposition alongside yield commentary. Mainstream financial coverage, by contrast, often quotes DGS10 in isolation, treating it as a single signal. This asymmetry between professional and retail-facing analysis is itself a marker of the gap between informed and uninformed reading of yield moves.

4. Limits of the breakeven proxy

T10YIE is not a pure measure of inflation expectations, and three gaps deserve to be known. First gap: T10YIE includes an inflation risk premium — the compensation demanded by nominal holders for bearing the risk that inflation deviates from the central scenario. This premium varies by regime; it is typically positive (15 to 50 bps) and increases with inflation uncertainty.

Second gap: T10YIE is biased by a TIPS liquidity premium. TIPS are structurally less liquid than nominal Treasuries, pushing their yield (DFII10) up and therefore T10YIE down. In market stress periods, this liquidity premium can spike and substantially distort T10YIE. September 2008 and March 2020 saw TIPS dislocations that made breakevens artificially low.

Third gap: T10YIE averages anticipated inflation over 10 years, without visibility on the intra-period trajectory. A 2.3% T10YIE can correspond to a “3% for five years then 1.6% for five years” trajectory, or to a stable 2.3% trajectory over the decade. The breakeven curve (T10YIE versus 2-year, 5-year, 30-year breakevens) partially reconstructs the trajectory but remains imperfect.

A fourth methodological limit deserves flagging. DFII10 measures the ex-ante real yield of a TIPS that indexes its coupons and principal on urban CPI (CPI-U, the Bureau of Labor Statistics series). The T10YIE breakeven is therefore the CPI-U inflation expectation, not a more fundamental measure like the PCE deflator that serves as the Fed’s official target. The structural CPI vs PCE gap being historically 30 to 50 bps (CPI overweights housing while PCE integrates basket substitutions), one must mentally translate T10YIE for comparison with the Fed’s 2% PCE target. A complementary angle: our decoding of the copper-gold ratio as a leading signal.

For these reasons, some analysts prefer zero-coupon inflation swaps as a purer proxy for inflation expectations. The swap removes the TIPS liquidity premium but introduces its own biases (counterparty risk, market segmentation). In practice, rigorous reading cross-references T10YIE and inflation swap to identify episodes where the gap between the two indicates TIPS dislocation rather than an authentic expectations revision.

Reading T10YIE as “pure inflation expectation” and using its variations as a direct inflation-pricing indicator. T10YIE is a combination of mean expectation, inflation risk premium, and a TIPS liquidity premium bias that inverts its signal in Treasury stress phases (March 2020, October 2008). To isolate true inflation expectations, cross-reference T10YIE with the 10-year zero-coupon inflation swap and look at episodes where the two diverge.

Last updated — 12 July 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

Full pillar →Real Rates: The True Cost of Capital Is Repricing

Why real rates are reasserting themselves as markets' anchor and how to recalibrate investment and financing decisions facing…

Real Interest Rates: The Quiet Signal Reshaping Markets

Real interest rates: why their persistence in positive territory in 2026 is reshaping the rules for bonds, equities,…

OAT-Bund Spread: A Quiet Gauge of French Sovereign Risk

OAT-Bund spread: how this yield gap has become a key signal on French sovereign risk, fiscal policy and…