Euro Funds in Life Insurance: Still Useful in 2026?

Euro funds in French life insurance regain strategic relevance in 2026 amid positive real rates and renewed market volatility. Their role: securing capital, absorbing shocks and structuring long-term allocation.

Euro funds in French life insurance contracts are regaining strategic relevance in an environment where real rates have turned positive again. They do not aim for maximum performance, but for wealth stabilization and risk smoothing.

TL;DR

French net life-insurance inflows topped €50bn in 2025, a 15-year first: with real returns turning positive (~2.5% net vs ~1% inflation), euro funds regained their role as a stability anchor. See also our comparison of traditional and Roth accounts.

- In 2025, euro funds averaged 2.5–2.65% net of fees (Facts & Figures, L'Argus); after 17.2% social contributions and ~1% French inflation, the net real return reached roughly +1.2%, the first positive reading since 2016.

- Eight ECB rate cuts took the deposit facility from 4% to 2% (June 2024–June 2025), while insurers reinvest bond portfolios at 2.5–4% on 5–15-year maturities — a rollover effect that lifts distributed returns with multi-year inertia.

- Profit-sharing reserves (PPB) that smooth payouts fell from 4.41% to 3.91% of assets between end-2023 and end-2024 (Mingzi), widening dispersion between insurers.

- Realized 2025 payouts ran from under 2% (worst contracts) to over 3.5% (best mutuals), while the Livret A dropped to 1.5%, below the better euro funds.

Between disinflation, higher bond yields and renewed market volatility, their role is shifting: securing a portion of savings, absorbing shocks and structuring long-term allocation.

Euro funds in life insurance: how they are used effectively in 2026 to secure capital, smooth risk and optimize long-term savings. This dynamic is mapped out in our comparison of euro funds and bond ETFs against rates.

Euro funds in life insurance: a vehicle once again strategic

With euro area inflation falling to 1.7% in January 2026 and French 10-year sovereign yields around 3.4%, euro funds in life insurance are regaining a position they had not held since the 2000s. Returns paid for 2025, published in early 2026, average around 2.50–2.65% net of management fees according to consultancy Facts & Figures and L’Argus de l’Assurance, with considerable dispersion: under 2% for the worst-performing contracts to over 3.50% for the best mutuals.

Understanding this shift requires placing euro funds within a broader savings strategy rather than treating them as a “second savings account”. Readers who want to first master the general framework of financial education and the main investment vehicles may prefer to consult that resource before exploring finer trade-offs.

What is changing quietly: after eight policy rate cuts between June 2024 and June 2025 (the ECB brought its deposit facility from 4% to 2%), insurers hold bond portfolios reloaded at significantly higher rates than during 2015–2021. Combined with inflation now under control, this new regime alters the optimal place of euro funds within a portfolio.

How a euro fund actually works in 2026

A euro fund is a life insurance vehicle with capital guaranteed by the insurer (absent insolvency), invested mainly in government and corporate bonds (around 80% on average), with a smaller share of equities and real estate. Three key mechanisms determine returns:

- The legacy bond stock: sometimes acquired at very low rates between 2015 and 2021, these bonds still weigh on average performance — but their share diminishes as they mature and are replaced by better-yielding securities.

- New purchases at higher rates: since 2022, insurers have been reinvesting at 2.5–4% on 5–15-year maturities. This rollover effect is the main driver of the improvement in distributed returns.

- Reserves (profit-sharing provisions, PPB): set aside in “good” years and redistributed later to smooth returns. According to Mingzi, average reserves moved from 4.41% at end-2023 to 3.91% at end-2024. The level remains adequate on average but masks significant disparities between insurers: some drew heavily on their reserves, others rebuilt them.

Projections for 2026 anticipate gross returns around 2.5–2.8% on average according to Meilleurtaux Placement, supported by sustained high bond yields and strong inflows. But this average masks, as in 2025, sharp differences between contracts.

Why the macro context makes euro funds strategic again

Between 2015 and 2021, with French 10-year sovereign yields often near 0%, euro funds delivered net returns barely above 1%. In 2022–2023, euro area inflation still averaged above 5% annually: the real return on euro funds was deeply negative. According to Facts & Figures, performance net of inflation and social contributions remained negative every year between 2017 and 2023. On the same theme: our reading of guaranteed vehicles once prices are netted out.

By early 2026, the picture had changed:

- Euro area inflation down to 1.7% in January 2026 (Eurostat), below the ECB’s 2% target — and only around 1% in France over 2025, according to preliminary estimates.

- A/AA-rated 5–10-year sovereign bonds: coupons typically between 2.5% and 3.5% depending on country. The French 10-year OAT trades around 3.4%, providing solid support for future euro fund returns.

- Equity markets more volatile since the rate rise and amid geopolitical uncertainty (global trade tensions, uncertain French fiscal policy).

This suggests a well-managed euro fund can now deliver a clearly positive real return — on the order of +1 to +1.5 points above French inflation in 2025, according to UFC-Que Choisir — while smoothing volatility in the rest of a portfolio. It is not spectacular, but it marks an important pivot: for the first time since 2016, “capital protection” no longer comes with a silent erosion of purchasing power.

This anchor function is often poorly understood because it is analyzed in isolation. As shown in the reference article on structuring financial decisions over time, the value of a low-volatility vehicle like a euro fund does not come from its return alone, but from its place in the sequence of wealth choices: securing first, stabilizing next, then only taking on risk exposure.

The real saver question: how much to place in a euro fund?

What many readers are really asking is whether the era of placing “everything” in a euro fund is definitively over, or whether this vehicle can still be central. The answer is nuanced: the euro fund is no longer a stand-alone investment, but it remains a liquidity and stability anchor for structuring the rest.

One signal worth noting: net life insurance inflows exceeded €50 billion in 2025, a first in 15 years according to France Assureurs, on total outstanding assets of more than €2,000 billion (around 70% of which in euro funds). This confirms that French savers have grasped the regime change — even if many continue to underestimate performance gaps between contracts.

Three uses emerge in practice:

- Medium/long-term safety cushion: the equivalent of an extended precautionary buffer (12–24 months of expenses) complementing a current account and regulated savings — all the more relevant since the Livret A dropped to 1.5% in early 2025, well below the best euro funds.

- Buffer zone within a risky portfolio: reducing the equity/ETF share without exiting the life insurance wrapper entirely.

- Reservoir for rotating into unit-linked supports (ETFs, SCPIs, equity funds) when markets correct.

Practical anchor points for using euro funds in 2026

1. A simple allocation framework

For a reader who already holds an emergency savings account and an initial equity portfolio, one possible framework is:

- Conservative profile: typically around 50% in euro funds, 30% in short bond/money market ETFs, 20% in equities/equity ETFs.

- Balanced profile: typically around 30% in euro funds, 20% in bonds/money market, 50% in equities/equity ETFs.

- Dynamic profile: typically around 15–20% in euro funds, 15% in bonds/money market, 65–70% in equities/ETFs and risk assets.

Central assumption: an investment horizon of at least 8 years and the capacity to absorb temporary drawdowns on the equity portion. The euro fund then acts as “ballast” to dampen shocks, complementary to equity and ETF supports.

2. Three signals to identify a good euro fund

Rather than chasing “last year’s best rate”, three indicators tend to be more useful:

- Five-year average return (2021–2025): a fund that maintained 2–2.5% over this period (including low-rate years and the subsequent rise) likely has more active management and better-calibrated reserves.

- Reserve level (PPB): the higher as a percentage of assets, the more the insurer can smooth future returns. Note: average reserves declined (from 4.41% to 3.91% between end-2023 and end-2024), making this criterion more discriminating.

- Entry fees: in 2026, accepting more than 1–2% entry fees on a euro fund has lost its rationale. The benchmark is 0% or close — the standard for online contracts (Linxea, Fortuneo, Boursorama).

An additional point of vigilance: a growing number of insurers condition their best rates on a minimum unit-linked share (often 20–30%, sometimes more). As UFC-Que Choisir notes (February 2026 ranking), this practice transfers part of the financial risk to the saver in exchange for a “boosted” return. Verifying that the unit-linked share corresponds to a genuine investment strategy — and not merely a gate to access the bonus — matters significantly.

3. KPI to monitor: net real return

The main indicator to monitor each year is straightforward:

- Net real return = distributed rate net of fees and social contributions – annual inflation.

A concrete example for 2025: with a euro fund delivering 2.65% gross (the market average), or about 2.19% net of social contributions (17.2%), and French inflation around 1%, the net real return comes out at approximately +1.2%. This marks a significant reversal compared with 2017–2023, when this same calculation systematically produced a negative result. For the best funds (3.00–3.50% gross), the net real return reaches 1.5–1.9%. The same net-of-cost reasoning, applied to annuity products charge by charge, is itemised in the fee stack inside variable annuities.

What consensus misses about euro funds

Part of the consensus continues to expect a structural decline in the appeal of euro funds, on the grounds that capital protection has become too costly to offer and that returns will remain compressed. The implicit conclusion: a massive shift toward unit-linked supports is required. Insurers themselves reinforce this reading by conditioning their best returns on rising unit-linked shares.

The reading here diverges on one precise point: the euro fund is becoming less a performance product than a sequence-risk management tool. In other words, it serves to avoid having to sell equities at the worst moment (crash, recession) to fund a project or expense. Even with moderate returns, its value derives from this shock-absorber function in a turbulent economic cycle marked by recurring geopolitical shocks and more volatile rates.

The 2025 record provides a concrete illustration: euro funds delivered stable positive returns without volatility, while equity markets experienced bouts of turbulence linked to global trade tensions and European fiscal uncertainty. For a saver who needed liquidity at a moment of market stress, the euro fund pocket made precisely the difference.

A less obvious reading sees euro funds as the “enhanced cash” of financial wealth, reconciling safety and medium-term return rather than serving as a flagship product.

Common mistakes with euro funds

Mistake 1: placing everything in a euro fund “for safety”. This is misleading because, over 15–20 years, even a +1% real return is insufficient to build significant wealth. The correct reading: the euro fund is a stability anchor, not a primary engine of wealth growth.

Mistake 2: switching contracts solely for 0.2 points of additional return. Focusing on a one-year gap isolates a misleading indicator. Overall contract quality matters more (fees, unit-linked options, insurer solidity, five-year return history), along with consistency with the broader wealth strategy. Within that broader planning, how the contract passes to the people named on it is a separate matter, addressed in beneficiary designations on inherited accounts.

Mistake 3: being lured by “unit-linked bonuses” without measuring the risk. Accepting 30–60% in unit-linked supports to obtain +0.5 to +1 points of additional euro fund return is only rational if that unit-linked share matches a long horizon and a genuine risk tolerance. Otherwise, the saver transfers risk unwittingly — a pattern La Finance pour tous and UFC-Que Choisir highlight in their February 2026 analyses.

Mistake 4: ignoring the impact of rates and the macro cycle. A euro fund does not react instantaneously to rate moves: the 2022–2023 rise continues to feed through bond portfolios over several years. Conversely, if long-term rates were to fall significantly, distributed returns would take time to erode — the inertia cuts both ways. Underestimating this lag leads either to a hasty conclusion that “euro funds are dead” or, on the contrary, that they have become miraculous.

Two plausible scenarios for 2026–2028

Scenario 1: rate plateau and contained inflation (central scenario)

Assumptions: the ECB holds policy rates around 2% (status quo confirmed on February 5, 2026, for the fifth consecutive meeting), with a possible modest cut in H2 2026 if inflation remains below 2%. The 10-year OAT oscillates between 3% and 3.5%. Modest growth in the euro area (GDP rose 1.5% in 2025 according to Eurostat).

Consequence: euro fund returns converge toward around 2.5–2.8% gross over the period, with positive inertia from gradual portfolio bond renewal. Net real return remains positive as long as inflation stays below 2%. The euro fund retains its shock-absorber role, competitive against the Livret A (1.5%) and certain short-duration bond funds. Placing such a conservative anchor on a lifecycle path, chosen for the saver or by the saver, is mapped out in delegated versus self-directed glide paths.

Scenario 2: inflation rebound or long-end yield stress

Assumptions: an energy shock, geopolitical tensions, or French fiscal strains push the 10-year OAT above 4%. Inflation rebounds toward 3–4% in 2027. The Observatoire Crédit Logement points to a risk of mortgage rates around 4% by end-2027.

In this case, euro funds suffer in the short term on the book value of their bond portfolios, but smoothing mechanisms and reserves cushion the shock for the saver. Over 3–5 years, if insurers can reinvest at higher rates, distributed returns eventually recover. The main risk for the saver would be exiting massively at the wrong moment — or seeing real return turn negative again if inflation sustainably exceeds the distributed rate.

Conversely, an accelerated easing scenario (the ECB resumes cuts, lending rates drop toward 2.5%) would be favorable in the short term for existing euro funds (portfolio bonds gain in value) but would progressively weigh on future returns as reinvestments occur at lower rates.

Deciding now: act or wait?

Behind the question “euro fund or not?” lies a simpler concern: “Am I missing out on better returns elsewhere, or taking unnecessary risk?” The right approach is less binary.

- It is neither too late nor urgent to shift everything into a euro fund: the rebound in returns is already largely priced in, and 2026 projections extend the 2025 trajectory.

- The challenge lies in structuring savings: defining what share should remain risk-free, then allocating euro funds first within that share, alongside short-term cash — bearing in mind the Livret A at 1.5% now sits clearly below the best euro funds.

- Finally, it requires clarifying the horizon: the longer it is, the more the equity/ETF share can grow, and the more the euro fund share can concentrate on its cushion role.

Practical markers for three profiles

For retail investors

- Allocations between 15% and 50% of life insurance to one or more euro funds are common depending on risk tolerance and horizon.

- A progressive rotation (monthly or quarterly) from the euro fund toward equity ETFs during market correction phases of -10% to -20% is a documented practice.

- Monitoring the net real return of the euro fund annually and adjusting it against the broader wealth/real estate/retirement strategy fits within a wider reflection on long-term investment strategies.

For companies (excess treasury via capitalization contracts)

- Vehicles close to euro funds are used to smooth returns on stable treasury (cash not expected to be used within 3–5 years).

- Sizing typically remains limited to amounts that do not jeopardize operational liquidity under shock (customer payment delays, revenue drops).

- Systematic comparison: post-tax net return, accounting constraints, money market and short-bond alternatives.

For investors already heavily exposed to equity markets

- Treating the euro fund as a tool for reducing overall volatility: reinforcing the “cushion” in case of a crash without necessarily reducing the equity share.

- A minimum 10–20% pocket of very low-volatility assets (euro funds + money market) is commonly observed for weathering prolonged drawdown phases.

- Weak signals worth monitoring: bond spread tension (the OAT–Bund spread remains a focal point), volatility spikes, global trade tensions — as many indicators that the “safe” portion of the portfolio will soon be called upon.

Frequently asked questions on euro funds in 2026

Can euro funds still beat inflation over 10 years?

For the first time since 2016, the real return on euro funds turned clearly positive in 2025 (around +1 to +1.5 points above French inflation). If inflation stabilizes around 1.5–2% and returns hold around 2.5–3% gross, real return could remain positive over the period. But nothing guarantees it: a return of inflation or an erosion of bond yields would change the picture.

Are several contracts needed to diversify euro fund holdings?

Beyond €50–100k in assets, holding two different insurers limits concentration risk. It also allows access to different management policies (reserve levels, allocation, fees). The gap between the best and worst classic euro fund easily reaches 1.5 points in 2025 — which alone justifies diversification.

Is investing massively in a euro fund at once risky?

The main risk is not volatility but opportunity cost: locking in a sizable amount at a moment when other assets (equities, long bonds) offer a better long-term risk/return profile. Spreading deposits over 6–12 months can be more suitable.

Are “unit-linked bonuses” truly advantageous?

It depends on the profile. Accepting 30% in unit-linked supports for +0.5 points on the euro fund can be relevant if that share corresponds to an equity allocation consistent with the horizon. But for a saver seeking no risk exposure, the “bonus” amounts to taking risk on 30% of capital to marginally improve the return on the remaining 70%. Contracts without unit-linked constraints delivering 3%+ (such as certain mutuals: CARAC, MIF, France Mutualiste) warrant priority examination. In the same vein: our study on everyday financial trade-offs across economic regimes.

What happens if rates fall sharply from 2026 onward?

Bonds already in portfolio gain value, but new ones will be bought at lower rates. In the short term, euro funds can maintain solid returns thanks to the stock effect; in the medium term, performance gradually tapers. This is the model’s inertia: it protects on the way up and on the way down.

In summary: using euro funds effectively

Euro funds in life insurance are no longer the obvious one-size-fits-all investment they were in the 2000s, but they are not a relic to be discarded either. The central scenario today is not that they return to the heart of wealth performance, but they remain a discreet and structuring link in the overall strategy — all the more so since they now offer, for the first time in nearly a decade, a meaningfully positive real return.

Markets do not fully price this possibility: an unspectacular vehicle can substantially improve risk tolerance, and therefore the capacity to hold more volatile investments over time. In a world where shocks are more frequent than 15 years ago — trade tensions, fiscal uncertainty, geopolitical volatility — it is often this “boring” detail that distinguishes an investment plan that holds from one that breaks.

- Three takeaways

- In 2026, euro funds in life insurance return as a genuine stability anchor with a positive real return, thanks to reloaded bond portfolios and contained inflation — a reversal from the 2017–2023 period. The mechanics are set out in the guaranteed-vs-market balance by regime.

- The right reflex is not to place everything in a euro fund, but to use it for the share of wealth dedicated to safety and to smoothing market jolts, while checking that the chosen contract does not condition the return on unwanted risk-taking.

- The KPI to monitor is not the distributed rate alone, but the net real return after inflation and social contributions, integrated within a broader equities/bonds/cash allocation.

Last updated — 12 July 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

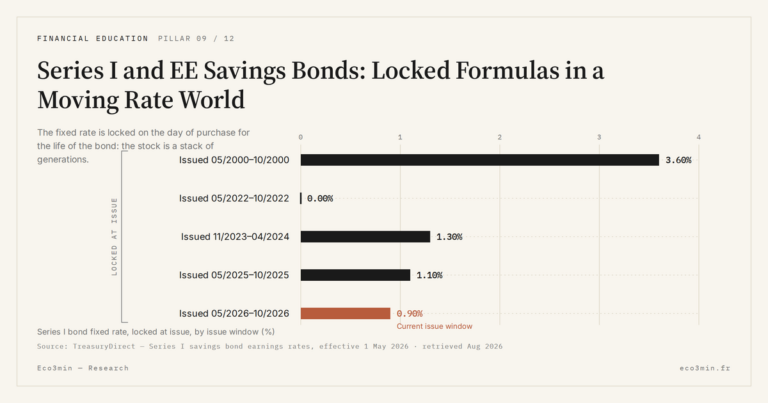

Full pillar →Series I and EE Savings Bonds: Locked Formulas in a Moving Rate World

US savings bonds lock a rate formula at the moment you buy them, for the life of the…

Where the Livret A’s Money Goes: The Caisse des Dépôts Circuit and Social-Housing Finance

The savings held on Livret A accounts do not sit idle. A regulation-set share is centralised at the…

France’s LEP vs the Livret A: A Means-Tested Higher Rate, Explained

France’s Livret d’épargne populaire is often described as "the Livret A, only better". The description misleads: the LEP…