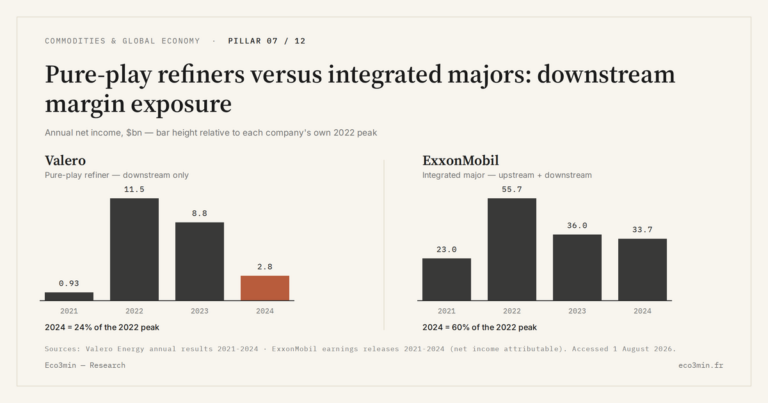

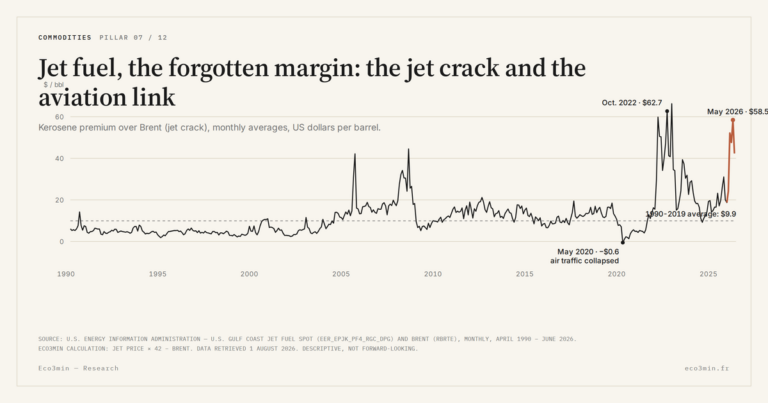

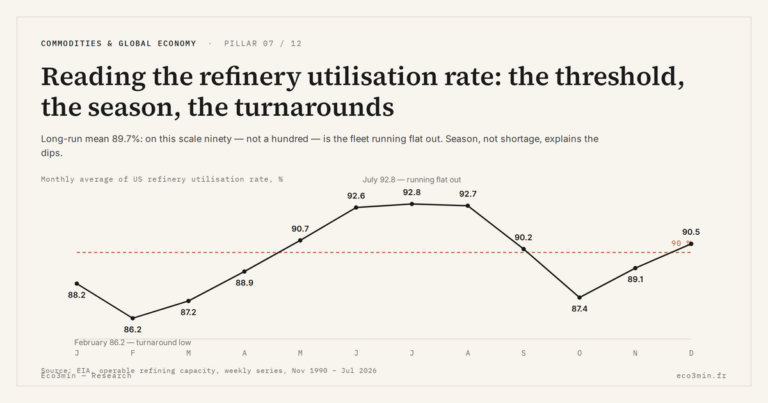

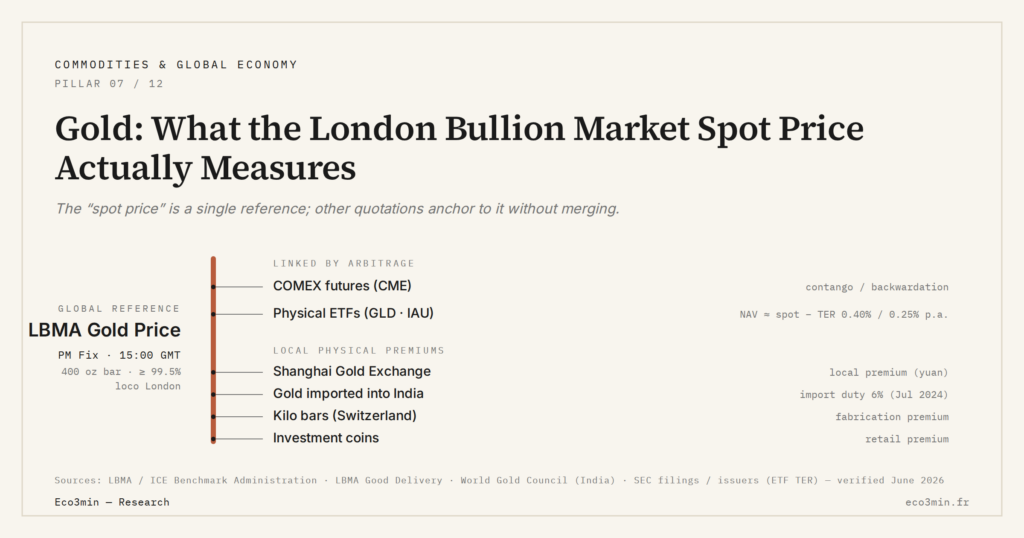

Gold: What the London Bullion Market Spot Price Actually Measures

The global reference gold price is not a single live datapoint but an institutional fixing produced twice daily in London, calibrated against a precise bar format and a precise delivery standard.

TL;DR

What retail sites show as one live gold number is really a bundle of quotations anchored to one global reference: the twice-daily LBMA Gold Price auction on 400-ounce good-delivery bars.

- Good-delivery gold means 400 troy-ounce bars at 99.5% minimum fineness from one of roughly seventy listed refineries, held loco London in LBMA-approved vaults that totaled around 8,500 tonnes at end-2024.

- Spot LBMA, 100-ounce COMEX futures and physical ETFs (GLD, IAU) track by arbitrage yet diverge: GLD's ~0.40% annual expense ratio compounds a measurable drag versus raw spot over a decade.

Understanding the quotation mechanic is a prerequisite for reading any long historical gold series, and for comparing the spot, futures and ETF markets coherently.

On most retail financial websites, the gold price is displayed as a single number updated in real time. That presentation conceals a more structured reality: the gold price is a bundle of quotations, of which only one serves as the global reference — the LBMA Gold Price administered by the Intercontinental Exchange Benchmark Administration. Every other quotation — COMEX futures, physical ETF shares, Shanghai Gold Exchange local premiums, kilo-bar premiums — anchors to that reference through arbitrage without merging with it. Understanding the exact perimeter of this fixing is a prerequisite for any serious macro analysis of the series, and more broadly for the full reading of gold as a monetary signal.

1. From the 1919 Telephone Fixing to the 2015 Electronic LBMA Gold Price

The London gold fixing is one of the oldest modern financial benchmarks. The London Gold Fixing was born on September 12, 1919, under the auspices of five London bullion houses — N M Rothschild & Sons, Mocatta & Goldsmid, Pixley & Abell, Samuel Montagu & Co, and Sharps Wilkins — which set up a daily telephone mechanism to fix a single reference price for refiners, banks and official treasuries. The arrangement initially ran once a day, then twice from 1968 onward. The composition of the five members evolved over the century but the format remained stable until the early 2010s.

The break comes in 2015. On March 20, 2015, the telephone fixing ceases and the LBMA Gold Price administered by the Intercontinental Exchange Benchmark Administration replaces it with an electronic auction mechanic. The transition follows the post-Libor regulatory reforms of 2012-2014, which demanded greater transparency and auditability of financial benchmarks. The practical consequence for readers of long series is that prior to March 2015 the published quotation is the London Gold Fixing, and after that date the IBA-administered LBMA Gold Price. The two series splice without major methodological rupture, but the underlying operational mechanic has changed substantially.

2. Auction Mechanic: AM Fix, PM Fix, and the 10,000-Ounce Tolerance

The LBMA Gold Price is set twice daily: AM Fix at 10:30 GMT, PM Fix at 15:00 GMT. The FRED series GOLDPMGBD228NLBM used in macro analysis reports the PM Fix exclusively, available daily since April 1, 1968 — this is the series underlying all gold-dollar, gold-TIPS, and gold-CPI correlations referenced on Eco3min.

The auction works in successive rounds. At the opening of each session, the IBA publishes a candidate price. Direct accredited participants — currently twelve to fifteen bullion banks including HSBC, JPMorgan, ICBC Standard Bank, Standard Chartered, Goldman Sachs, UBS, Morgan Stanley, Bank of China, Toronto-Dominion Bank, Bank of America, and Société Générale — declare in each round their buying or selling interest in ounces. If the gap between aggregate supply and demand exceeds 10,000 troy ounces, the IBA adjusts the candidate price and opens a new round. The sequence stops when the gap is below the tolerance threshold: that equilibrium price becomes the published LBMA Gold Price for the session. Each round typically lasts thirty seconds; a complete session reaches equilibrium in four to eight rounds, two to five minutes depending on market conditions. Background: how bullion, ETFs and miners compare.

This mechanic has two analytically important properties. First property: the resulting price is not a transaction price but a virtual equilibrium price at time T; declared orders settle contractually at the final price, and all participants clear their net flows at this single price. Second property: post-trade transparency is markedly higher than under the prior telephone fixing; aggregated session volumes are published.

3. The Good Delivery Perimeter: 400 Ounces, 99.5% Purity, London Delivery

The LBMA Gold Price applies to a strictly defined physical object: good delivery gold under LBMA standards. Concretely, this means bars of 400 troy ounces nominal (about 12.4 kilograms), with a minimum fineness of 99.5% gold, cast by a refinery listed on the LBMA Good Delivery List. That list comprises roughly seventy refineries worldwide and is dominated by the Swiss hubs — Valcambi, PAMP, Argor-Heraeus, MKS PAMP — which refine a majority share of global mine output. Other listed refineries are located in the United Kingdom (Asahi Refining UK), Japan (Tanaka Kikinzoku), Australia (Perth Mint), Russia (Krastsvetmet, Prioksky), South Africa (Rand Refinery) and the United States (Asahi Refining USA, Metalor USA).

Delivery is effected loco London: the gold is physically deliverable in an LBMA-approved vault in London, principally HSBC, JPMorgan, the Bank of England (for official accounts), ICBC Standard, or in deliverable equivalent within the vaults of participating banks. The system operates via allocation and book-entry: the vast majority of transactions trigger no physical bar movement, only an allocation transfer between vault accounts. The total physical stock in LBMA-approved London vaults has been published monthly by the LBMA since 2017; it oscillated around 8,500 tonnes at end-2024.

4. Spot LBMA, COMEX Futures, Physical ETFs: Three Linked but Distinct Prices

Three markets quote gold simultaneously on a global scale, with continuous arbitrage between them yet none merging with the others. The LBMA spot market, measured by the London Fix twice daily and quoted continuously off-fix by participating market-makers. The futures market on COMEX (CME Group), with standardized contracts of 100 troy ounces, monthly maturities, and possible but minority physical delivery — the vast majority of positions being closed by offset before expiry. The physical ETF market, dominated by SPDR Gold Shares (GLD, launched in November 2004 by State Street and the World Gold Council) and the iShares Gold Trust (IAU), which hold gold physically in allocated vaults and issue shares backed by approximately one-tenth of an ounce each. For context: The respective share of ETFs, central banks and jewelry in demand.

The three prices are linked by arbitrage but differ. The LBMA spot is the reference; COMEX futures quote with mild contango under normal regimes — a futures price slightly above spot, reflecting storage costs and financing opportunity cost — and flip into backwardation in episodes of physical stress. ETFs quote a NAV very close to spot but with a bid/ask spread and a total expense ratio (TER) accrued daily: GLD charges roughly 0.40% per year, IAU roughly 0.25%. Over a decade, ETF share returns therefore accumulate a visible drag versus raw spot performance.

5. What the Quotation Leaves Out: Local Premiums and Physical Spreads

The LBMA Gold Price is the global reference, but it does not capture the totality of the physical market. Several local deviations coexist durably with the reference price without contradicting it. Worth reading alongside: our sub-pillar on the physical leg of commodities.

The Shanghai Gold Exchange quotes gold in yuan with a local premium known as the Shanghai premium, which has oscillated between -2 and +50 dollars per ounce since 2015. This premium reflects supply-demand conditions specific to the Chinese market (import restrictions, seasonal jewelry demand, refining capacity), as well as yuan-dollar exchange frictions. Gold imported into India carries an import duty premium that stood at 12.5% before 2024 and was reduced to 6% in July 2024 under the Indian federal budget. Swiss kilo bars — the format preferred by Asian markets — quote with a manufacturing premium of a few dollars per ounce over the 400 oz good delivery bar, reflecting recasting and remarking costs at Swiss refineries.

Jewelry demand and investment coins carry sometimes substantial manufacturing premiums: a South African Krugerrand or a Canadian Maple Leaf can quote 3% to 8% above spot depending on retail market liquidity. These local premiums do not contradict the LBMA reference but signal that the single global price is a construction: useful, robust, but imperfect at capturing actual physical dispersion. Macro analysts must keep this in mind to avoid over-interpreting an LBMA spot variation as a global regime change, when a local premium may absorb or amplify the signal.

This quotation mechanic remains the entry point to reading gold across long series, covered in gold’s major cycles since Bretton Woods. To situate these quotations within the broader physical-markets ecosystem, the page on physical commodity markets aggregates connected analyses on oil, gas, copper and critical minerals. The full FRED gold price series supports empirical inspection of every claim made in this article.

- The global reference gold price is the LBMA Gold Price (PM Fix at 15:00 GMT), administered by IBA since March 2015; the FRED series GOLDPMGBD228NLBM used in macro analysis is this same series, available since April 1968.

- The mechanic is a multi-round electronic auction engaging twelve to fifteen accredited bullion banks, with calibration via a 10,000-ounce tolerance on supply-demand balance.

- The price applies to LBMA good delivery gold: 400 troy-ounce bars, minimum 99.5% fineness, cast by a Good Delivery List refinery and deliverable loco London.

- LBMA spot, COMEX futures and physical ETFs are three markets linked by arbitrage but distinct; local premiums (Shanghai premium, India duty, Swiss kilo bars, investment coins) coexist durably with the reference without contradicting it.

Last updated — 12 July 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

Full pillar →Reading the refinery utilisation rate: the threshold, the season, the turnarounds

A refinery runs full near ninety percent, not a hundred: the last slice of nameplate capacity is a…

IMO 2020: the regulatory shock that rewrote product spreads

An environmental rule on marine sulfur can move a refining spread more than a swing in crude. IMO…

The 2022–2023 refining golden age: anatomy of an episode

In 2022, refined fuel prices climbed faster than crude. That gap, measured by the 3-2-1 crack spread, reached…