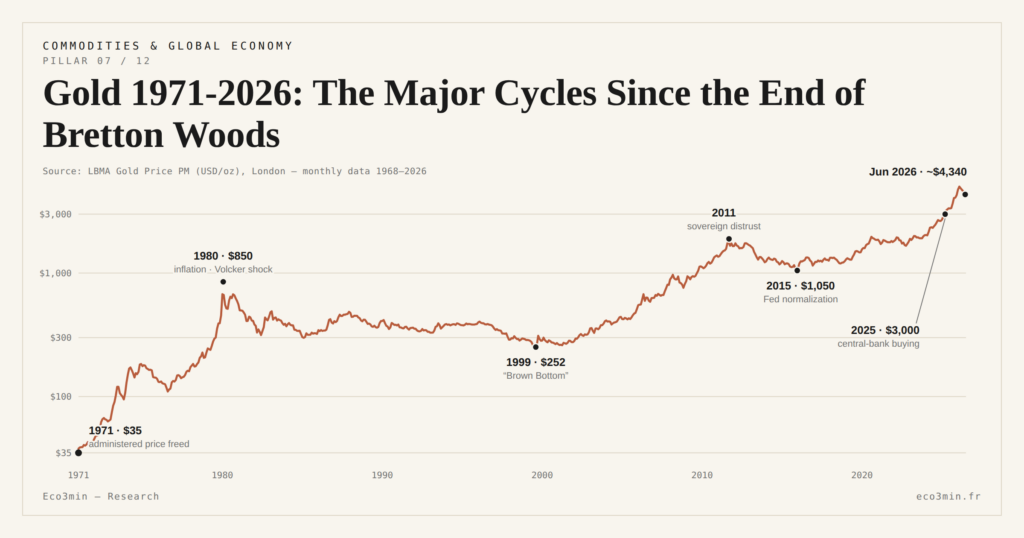

Gold 1971-2026: The Major Cycles Since the End of Bretton Woods

Since the unilateral end of dollar-gold convertibility announced by Nixon on August 15, 1971, gold prices have experienced four major cycles and three regime shifts, each carrying its own macro reading.

TL;DR

Four cycles and three regime shifts have shaped gold since Nixon ended dollar convertibility in 1971; the current one is the first to clear the 1980 peak in real terms.

- The 1971-1980 cycle ran from $35 to an $850 peak in January 1980, a 24-fold rise as US inflation reached 13.5%.

- The September 2011 peak of $1,923 marked a sovereign-distrust top rather than an inflationary one, coinciding with the first-ever US AAA downgrade and eurozone yields crossing 6%.

- In CPI-adjusted terms gold passed its January 1980 real peak in 2024; the $850 nominal high equates to roughly $3,200 in 2024 dollars.

The historical inventory of cycles is not a retrospective exercise: it provides the macro reference regimes indispensable for reading the current configuration.

Reading gold without a historical framework almost always leads to misinterpreting the present. The post-1971 trajectory has not been a linear climb: it organizes into four clearly identifiable cycles, each built around a dominant macro regime and bounded by datable inflection points. This structured inventory is a prerequisite to reading the current regime. For the synthesizing interpretive angle that mobilizes these cycles as backdrop, the master analysis of gold as a monetary signal proposes the three-driver grid; the present article supplies the underlying historical material. For the broader picture: gold against positive real rates.

1. August 15, 1971: The Inaugural Rupture and the Transition to Market Pricing

Before August 15, 1971, gold did not have a proper market curve: it had an administered price at $35 per troy ounce, guaranteed by the unilateral dollar convertibility for foreign central banks. That price had been set in January 1934 by the Gold Reserve Act under Roosevelt and maintained for thirty-seven years across World War II, the Bretton Woods reconstruction of 1944, and the monetary stability of the post-war boom.

On August 15, 1971, President Richard Nixon announces in a televised address the suspension of dollar-gold convertibility and the imposition of a 10% surcharge on imports. The decision is immediate, unilateral, and taken without consultation with monetary partners. It closes the Bretton Woods system and frees the gold price, which from that date becomes a freely traded asset on markets without institutional floor. The Smithsonian Agreements of December 1971 attempt a temporary compromise (gold reset at $38), then the Jamaica Accords of 1976 enshrine generalized currency floating. The London Fix, quoting at $35 in July 1971, reaches $197 in December 1974 — already nearly six times the pre-Nixon level. Companion analysis: the breakdown of gold demand across ETFs, official sector, jewellery and bars.

To situate this rupture within the context of modern quotation, the LBMA quotation perimeter explained precises the evolution of the reference benchmark; the 2015 transition from telephone fixing to electronic auction has preserved methodological continuity of long series since 1968.

2. The 1971-1980 Cycle: Inflation, Oil Shocks, the Imminent Volcker Peak

The first free cycle covers the nine years 1971-1980 and shows the strongest multiplication of the nominal price ever observed on the series: from $35 to a peak of $850 per ounce on January 21, 1980 (London PM Fix; intraday peak at $873 on some platforms), a 24-fold multiplication in under a decade.

Three drivers stack up. First driver: U.S. inflation, which rises from 3.3% in 1972 to peaks above 12% in 1974 and 13.5% in 1980 (BLS CPI historical series) — the most acute inflationary regime in modern U.S. history outside war periods. Second driver: the two oil shocks, the 1973-1974 one (post-Yom Kippur OPEC embargo, barrel quadrupled) and the 1979-1980 one (Iranian Revolution, barrel doubled). Third driver: growing distrust of the dollar and the international monetary system being rebuilt post-Bretton Woods, with flight to real assets amplifying self-fulfilling inflation expectations. Related coverage: how oil, gas and copper send structural signals.

The January 21, 1980 peak nearly coincides with Paul Volcker’s arrival as Fed Chairman (August 1979) and the FOMC’s October 1979 decision to target monetary aggregates rather than the Fed Funds rate — a major tightening signal that has not yet produced its effects on the gold price but marks the cyclical top.

3. The 1980-2001 Bear Cycle: Disinflation, Strong Dollar, Brown Bottom

The bear cycle that follows the 1980 peak is the longest and deepest in modern gold history. From $850 in January 1980, the price descends to $252 in August 1999 — a 70% loss in nominal terms and over 80% in CPI-adjusted real terms. Three drivers antagonistic to the prior cycle explain this durable decline.

First driver: Volcker tightening. Fed Funds are pushed to a 19% peak in July 1981, CPI inflation drops from 13.5% in 1980 to 3.8% in 1982, and inflation expectations are durably crushed. Second driver: structural disinflation that settles over the 1980s. Third driver: the strong-dollar reign initiated in the 1990s, extended under the Clinton administration (1993-2001) with the Strong Dollar Policy doctrine articulated by Robert Rubin and the Greenspan Fed.

The floor of this sequence sits in August 1999, at $252 per ounce — known as the Brown Bottom, after British Chancellor Gordon Brown, who then announces the sale of 395 tonnes of Bank of England gold reserves spread over 1999-2002. These official sales, conducted via seventeen public auctions at average prices around $275, were subsequently the target of extensive criticism in the United Kingdom — the timing being retrospectively perceived as near the cyclical minimum. The September 1999 Washington Agreements, which capped European central bank cumulative annual sales at 400 tonnes over five years, contributed to stabilizing the market from that floor onward.

4. The 2001-2011 Bull Cycle: Bubbles, GFC, the First QE Rounds

The third major cycle opens a decade of sustained climb: from $252 in August 1999 to $1,923 per ounce in September 2011, a 7.6-fold multiplication in twelve years (the cycle gains momentum from 2001 after a 1999-2001 stabilization zone). The drivers are diverse and stacked.

First driver: the succession of successive bubbles (dot-com 2000-2001, U.S. housing 2003-2007) and their chaotic resolution, degrading confidence in nominal assets and monetary policies. Second driver: the 2008-2009 global financial crisis, producing the sharpest systemic stress peak since 1929 and unleashing the first three Fed QE rounds (QE1 November 2008, QE2 November 2010, Operation Twist September 2011). Third driver: the degradation of the U.S. sovereign rating — on August 5, 2011, S&P strips the U.S. AAA for the first time in history (move to AA+), three days after a last-minute fiscal compromise avoiding technical default.

The September 6, 2011 peak ($1,923 LBMA PM Fix; intraday $1,920.94 on continuous spot markets) precisely coincides with the eurozone’s entry into the sovereign debt crisis: Italian and Spanish 10-year yields cross 6%, and systemic doubt about European public bonds generalizes. These two events — U.S. downgrade and eurozone crisis — illustrate that the 2011 peak is not an inflationary top but a sovereign-distrust top, distinguishing it qualitatively from the 1980 peak.

5. The 2011-2015 Bear Cycle: Anticipated Then Effective Fed Normalization

From September 2011 to December 2015, the price retreats from $1,923 to $1,050 per ounce, a 45% loss in four years. The primary driver is Fed normalization, anticipated by markets then enacted.

Three inflections structure this decline. First inflection: the May 22, 2013 taper tantrum, when Ben Bernanke first mentions the possibility of reducing QE3; the mere announcement triggers a 10-year TIPS yield climb of 80 basis points in six weeks, and an immediate gold pullback of over $200. Second inflection: the end of QE3, announced in October 2014. Third inflection: the first Fed Funds hike since June 2006, executed on December 16, 2015 at 0.25-0.50%.

The cyclical floor sits precisely around that final hike, at $1,050 in December 2015. Over this window, the two-variable grid — real yields plus dollar — works without interference: DFII10 rises from -0.5% to +0.7%, the DXY gains 25%, and gold retreats per the classical scenario. No other channel is mobilized to explain the move.

6. The Current Cycle 2015-2026: Structural Climb and Crossing the 1980 Real Peak

The cycle opening in December 2015 is not complete at the time of writing (May 2026). Its trajectory is marked by two successive regime shifts that make it qualitatively distinct from the three prior cycles.

First sequence: 2015-2020. Gradual climb from $1,050 to $1,700 in January 2020, then brutal acceleration under the Covid shock and the unlimited Fed QE response; the $2,000 threshold is crossed for the first time on August 4, 2020, with an interim peak at $2,075. Over this first sequence, the classical real yields plus dollar grid suffices broadly.

Second sequence: 2022-2026. From early 2022, the structural driver of massive central bank purchases activates — roughly 1,080 tonnes in 2022, 1,037 tonnes in 2023, projected 1,100 tonnes in 2024 per the World Gold Council. These volumes represent nearly a quarter of annual global demand and create an unprecedented structural price floor. The $3,000 per ounce threshold crossed in March 2025 fits this logic. For the detailed reading of this regime, the analytical singularity of the current $3,000+ regime specifically treats the three competing readings of the current level.

A peculiarity of the current cycle deserves a historical mention. In real terms — that is, adjusted by cumulative U.S. CPI — gold prices in 2024 exceeded their historical peak of January 1980. The $850 nominal peak of January 1980 equated to roughly $3,200 in 2024 dollars under standard CPI conversions; the clear surpassing of that level in real terms in 2024 then in 2025 makes the current cycle the first post-1971 bull cycle to erase the Volcker peak in both real and nominal terms. This specificity is documented precisely in the January 1980 peak in real terms exceeded, with supporting empirical inspection available via the real-terms gold price dataset.

To situate this cycle in the broader macro panorama, Eco3min’s analytical mesh connects several complementary readings: the oil burden and recession trigger reading illuminates the commodity-side cyclical anticipations that often express themselves in flows toward gold; and the page on the physical commodities and structural signals sub-pillar aggregates connected analyses of physical markets.

Treating the September 2011 nominal peak ($1,923) as the historical top of the long gold cycle empirically contradicts the data since 2020. The $2,000 threshold was crossed in August 2020, the $3,000 threshold in March 2025, and in CPI-adjusted real terms the January 1980 peak itself was exceeded in 2024. Reading every interim peak as a terminal top is a mono-causal projection that ignores regime breaks; the correct reading is cyclical and regime-dependent.

Last updated — 12 July 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

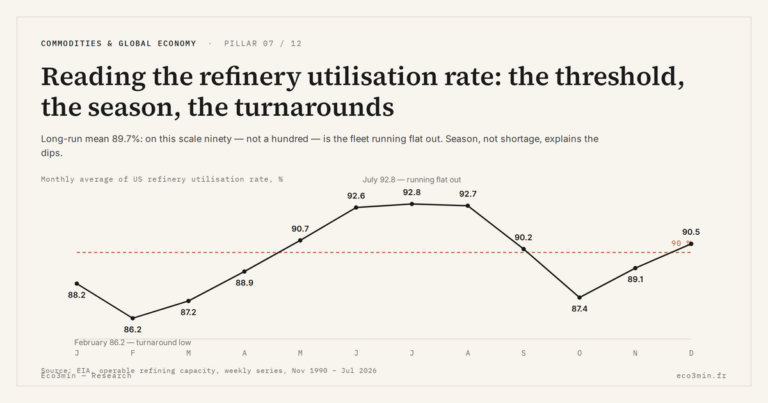

Full pillar →Reading the refinery utilisation rate: the threshold, the season, the turnarounds

A refinery runs full near ninety percent, not a hundred: the last slice of nameplate capacity is a…

IMO 2020: the regulatory shock that rewrote product spreads

An environmental rule on marine sulfur can move a refining spread more than a swing in crude. IMO…

The 2022–2023 refining golden age: anatomy of an episode

In 2022, refined fuel prices climbed faster than crude. That gap, measured by the 3-2-1 crack spread, reached…