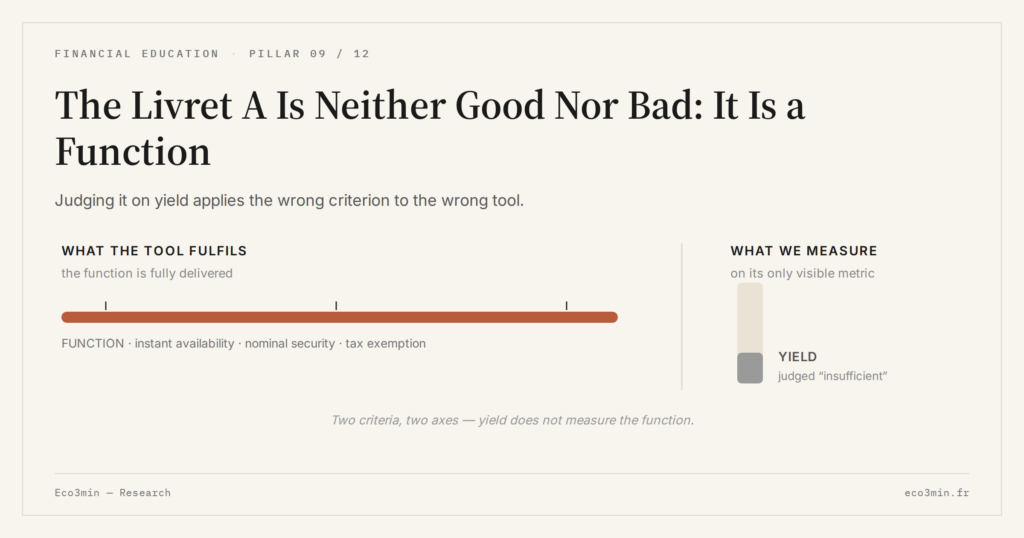

The Livret A Is Neither Good Nor Bad: It Is a Function

The Livret A serves a function of liquidity and nominal security. Judging it on yield confuses the tool with the objective.

The Livret A serves a function of liquidity and nominal security. Judging it on yield confuses the tool with the objective.

TL;DR

The Livret A is a liquidity and nominal-security tool: it guarantees instant availability, capital safety and tax exemption, while leaving purchasing power exposed when inflation runs above its rate. That role-versus-yield distinction is placed within the function-first reading of an account.

- Total Livret A and LDDS outstandings exceeded €580 billion at end-2025 (Caisse des dépôts), yet around 8% of accounts hold more than half of deposits (Banque de France), with balances well above precautionary-reserve needs.

- At a 2.4% rate in early 2026 against INSEE inflation projected at 1.5% to 2%, the real return turns slightly positive, a transitory configuration that does not change the tool's function.

Each time the Livret A rate is published, the same debate resurfaces: is it “enough”? The question is poorly framed. The Livret A — France’s flagship regulated savings account — is not a yield product. Eco3min sets out what that function implies in how administered savings rates interact with financial repression. It is a liquidity and nominal-security tool, designed to fulfil a precise function within a household balance sheet. Understanding that function makes it possible to use the instrument without overrating or dismissing it. Related work: our walkthrough of the tools that pressure-test assumptions.

What is often left aside: the issue is not the Livret A rate itself, but the framing that turns it into an object of permanent evaluation. As long as it is perceived as an investment to be judged, it will always feel “insufficient”. Related material: US Series I and EE savings bonds.

A Liquidity Function, Not a Yield Function

The Livret A guarantees three things: immediate availability of capital, nominal security, and full tax exemption on interest. These features define its function: a precautionary reserve, mobilisable at any moment, without tax friction. A related perspective: the line between a liquidity function and a defensive one. A companion piece: Compound Interest: Why Time Outweighs Yield in Finance.

According to data from the Caisse des dépôts (2025 annual report), total Livret A and LDDS outstandings exceeded €580 billion at end-2025. The behaviour of balances past the ceiling is examined in what happens to deposits above the Livret A cap. Yet according to Banque de France, around 8% of accounts hold more than half of total deposits, with balances well above any precautionary reserve need — a sign that part of the outstanding stock no longer fulfils the function for which the tool was designed.

Nominal security is real, but it does not protect purchasing power. When inflation exceeds the rate paid, capital loses value in real terms each month. This mechanism highlights the limits of the nominal-security concept — a guarantee on the figure, not on what it can buy.

The Wrong Criterion Applied to the Wrong Tool

Judging the Livret A on yield means applying an investment criterion to a savings tool. The confusion is widespread because yield is the only visible metric — the one the media report, the one savers compare. But the performance of a liquidity tool is not measured in annual percentage terms: it is measured in availability and absence of friction. Recognising the nature of each financial vehicle avoids projecting onto a product expectations that do not match its design. More context: Saving Is Not Investing: Why the Confusion Carries a Cost.

Media commentary swings between “the Livret A pays nothing” and “the Livret A is back to a decent level”. Both assessments make the same mistake: they treat yield as the primary criterion for a liquidity tool. A broader view: the US household cash and deposits mix.

Comparing the Livret A rate to inflation to conclude it “loses money”. The comparison is technically correct in real terms, but it applies a yield criterion to a liquidity tool. A precautionary reserve is not designed to beat inflation — it is designed to remain available. euro funds against unit-linked exposure places this dynamic within the cluster’s framework.

What the Current Rate Environment Reveals

In early 2026, the Livret A rate stands at 2.4%. According to INSEE projections (January 2026), French inflation is expected to stabilise around 1.5% to 2% over the year. The real return turns slightly positive again — an unusual configuration that may not last if the rate is revised lower in the second half. A dedicated resource: the major investment vehicles read by regime. Related framing: Investment Horizon: Why It Is the First Question, Not the Last.

What would invalidate this reading is the emergence of a product offering the same liquidity, the same nominal guarantee and a yield durably above inflation. Neither current market conditions nor the regulatory framework make such a scenario likely. The same mechanics are viewed differently in the article on What ’Placing’ Money Reveals About Risk Perception. A parallel read: high-yield savings versus money market funds after tax.

The Livret A is neither good nor bad. It is a liquidity tool whose relevance depends on the function assigned to it. Several rate scenarios remain open, but none alters this reading framework — a trade-off that fits within everyday savings choices.

- The Livret A serves a function of liquidity and nominal security — judging it on yield confuses the tool with the objective.

- The record outstanding stock suggests a significant share of deposits exceeds precautionary needs, without savers identifying it as such.

- The slightly positive real return in early 2026 is a transitory configuration — it does not change the function of the tool.

Last updated — 12 July 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

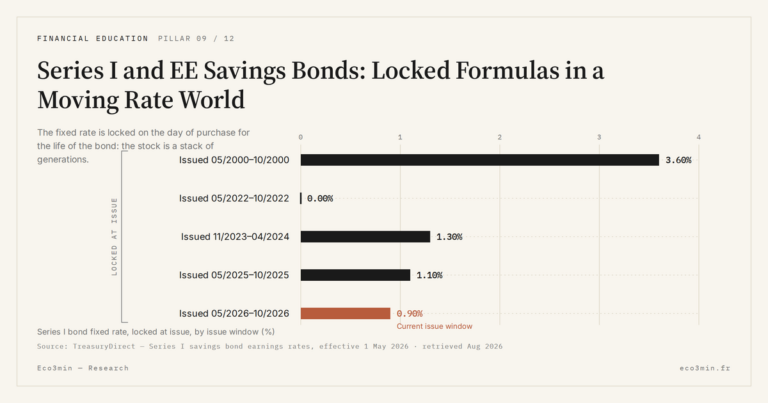

Full pillar →Series I and EE Savings Bonds: Locked Formulas in a Moving Rate World

US savings bonds lock a rate formula at the moment you buy them, for the life of the…

Where the Livret A’s Money Goes: The Caisse des Dépôts Circuit and Social-Housing Finance

The savings held on Livret A accounts do not sit idle. A regulation-set share is centralised at the…

France’s LEP vs the Livret A: A Means-Tested Higher Rate, Explained

France’s Livret d’épargne populaire is often described as "the Livret A, only better". The description misleads: the LEP…