WTI 2024-2026: The $70-85 Stabilization Regime and Volatility Compression

Since late 2023, WTI has traded in a narrow $70-85 corridor with realized volatility compressed to levels unprecedented outside crisis. Three structural readings coexist: slowed Chinese demand, U.S. shale as swing producer, U.S. SPR at only 50% capacity.

TL;DR

A $70-85 WTI corridor has held since late 2023 as three forces converge: Chinese demand caps the top, U.S. shale lifts the floor, a half-empty SPR skews shock response.

- On demand, China: growth down to +1.2% a year in 2023-2025 (EIA, IEA) from +4.5% over 2003-2019, with electric vehicles above 45% of Chinese new-car sales in 2024.

- On supply, shale: a $45-55 Permian break-even (Dallas Fed Energy Survey) damps moves both ways on a 6-to-18-month cycle, tempered by post-2020 capital discipline favoring buybacks over drilling.

- The SPR, near half capacity at ~370 of 714 Mb (DOE): thin draw-down room after 350 Mb pulled in 2021-2023, but about 344 Mb to buy back to refill, an asymmetric lever on shocks.

This piece maps the three readings. It does not rank them: each contributes to explaining the stabilization, and each carries a different durability horizon.

1. The $70-85 Stabilization Regime: Empirical Facts

Since October 2023, WTI has traded in a narrow corridor. Per FRED DCOILWTICO, over the October 2023 to May 2026 period, more than 85% of trading sessions occurred between $65 and $90, and more than 65% between $70 and $85 — unusual concentration for a commodity that historically traverses $50-amplitude corridors over two years. The average over the period is $77, the 90-day rolling standard deviation typically between $5 and $8, versus $12-18 over the 2010-2020 decade. The wider context: The relative dynamic of gold and crude oil.

WTI realized volatility over the same period is also compressed. Calculated as the annualized standard deviation of daily returns over a 30-day rolling window, it sits most of the time between 18 and 28% — versus a historical average of 35% over 1990-2020 and peaks above 100% in April 2020. The OVX (CBOE Crude Oil ETF Volatility Index) confirms this compression: 2024-2026 average levels below 30 versus a historical average around 40. For the equity-volatility analogue, see our VIX dataset.

The contrast with previous phases is sharp. Over 2010-2014, WTI traded between $75 and $110 with average realized volatility 25%. Over 2014-2020, the corridor widens considerably ($26 to $110) with episode-contrasted volatility. Over 2020-2023, after the COVID and Ukraine episodes, the corridor remains wide ($47 to $124). The post-October 2023 period is therefore a qualitative break: the first phase of prolonged stabilization in a narrow corridor since 2014.

Historical comparisons across longer periods give additional perspective. The early 2010-2014 corridor was a result of strong demand from China, an OPEC+ acting as cartel with little disruption, and a U.S. shale industry still ramping up. The post-October 2023 corridor emerges from very different conditions: weaker Chinese demand, a U.S. shale industry mature and disciplined, and an SPR partially drawn down. These different underpinnings make the current corridor structurally distinct, even though the empirical range happens to fall in a similar zone. The lesson is not that history repeats, but that similar empirical patterns can emerge from different structural configurations — which complicates inference from the surface description of the corridor to its expected persistence.

This compression is neither a prediction of a stable future nor a causal reading. It is an empirical description of the regime. For the role of this stabilization in U.S. macro, the reference is the cluster’s WTI as comprehensive macro signal which synthesizes the three analytical functions of the U.S. barrel. For the live WTI series tracked at daily frequency, see current WTI tracking on Eco3min.

2. Reading 1: Slowed Chinese Demand

The first reading emphasizes the structural slowdown of Chinese oil demand. Per EIA and IEA data, Chinese demand growth has returned to about +1.2% per year on average 2023-2025, versus +4.5% per year on average over 2003-2019. This deceleration is triple: slowdown of Chinese economic growth (shift from 6-7% per year pre-2019 to 4-5% post-2022), maturation of the auto fleet and shift toward electric vehicles (EVs represent more than 45% of Chinese new car sales in 2024 per BloombergNEF), and structural decline of heavy industry in favor of services.

Quantitatively, the growth gap is substantial. If China consumed 4.8 Mb/d in 2000 and 16.4 Mb/d in 2024, linear extrapolation at the +4.5% pace would have given a 2024 expected level substantially higher. This Chinese demand shortfall relative to the historical trajectory mechanically weighs on the global price, since China represents the principal source of incremental demand since 2000.

The durability horizon of this reading is intermediate. On one hand, the structural slowdown of Chinese growth is probably durable (demographic transition, end of the investment super-cycle). On the other hand, factors can reverse the trend: massive Chinese fiscal reflation, slowdown of EV adoption, idling of competing refineries. None of these reversals is inscribed in current data; none is excluded over a 2-3 year horizon either.

3. Reading 2: U.S. Shale as Swing Producer

The second reading emphasizes the role of U.S. shale as a swing producer capable of responding rapidly to price variations. Per Dallas Fed Energy Survey (quarterly survey of Texas, Louisiana, New Mexico operators), the average break-even for profitably bringing a new well online in the Permian basin is in the $45-55 range (2024-2025 figure), versus $60-75 in secondary basins (Eagle Ford, Bakken). This cost structure allows Permian operators to keep drilling even at WTI at $70, while being able to gradually slow down if the price falls below $60.

Shale dynamics act as a damping mechanism in both directions. When WTI rises above $90, operators accelerate drilling and production rises with a 6-9 month lag, bringing supply back to demand. When WTI falls below $65, drilling slows and cumulative production declines over 12-18 months (through natural decline of existing wells combined with the halt of new ones), bringing supply down and the price back up. This short-cycle mechanic, specific to shale, is very different from the long-cycle of traditional offshore projects (Brazil, Mexico, North Sea) which have production lead times of 5-7 years.

The durability horizon is tied to two factors. First, shale productivity per well drilled: productivity gains (lateral length, fracking optimization) have so far compensated for the decline of “sweet spots”. Dallas Fed reports 2024-2025 nevertheless signal a slowing of this productivity improvement. Second, capital discipline among public operators: since 2020, they have adopted a shareholder-return policy (dividends, buybacks) rather than aggressive drilling growth — moderating the supply response relative to earlier cycles.

To understand how this shale swing-producer role interacts with the structural WTI-Brent differential, the cluster addresses it in WTI-Brent spread in the current regime.

4. Reading 3: Partially Refilled U.S. SPR

The third reading emphasizes the state of the U.S. Strategic Petroleum Reserve. Per DOE (Department of Energy), the SPR was drawn down by 350 Mb (million barrels) between late 2021 and late 2023, in the context of Biden’s April 2022 decisions aimed at moderating prices after the Russian invasion of Ukraine. As of May 2026, the SPR contains about 370 Mb out of a maximum capacity of 714 Mb — about 52% of capacity utilized. The rebound from the mid-2023 trough of 347 Mb is modest, constrained by the federal budget and DOE-targeted purchase prices ($67-72).

The structural implication is dual and asymmetric. On one hand, the marginal draw-down capacity is limited: with only 370 Mb, a massive intervention like that of 2022 (180 Mb drawn in 6 months) would reduce the SPR below 200 Mb — historically low level. The capacity for rapid intervention in case of supply shock is therefore weakened relative to 2021. On the other hand, the refill capacity is substantial: to bring the SPR back to full capacity, about 344 Mb would need to be purchased on the market — significant demand flow that would constitute a mechanical floor on the price if refill accelerated. A complementary angle: our analysis of energy and metals as physical markets.

The durability horizon depends on political trade-offs. An administration wanting to accelerate the refill would buy above current prices, contributing to supporting the market. An administration less concerned with this objective would maintain the current slow pace. The SPR as a variable is therefore both a structural instrument (capacity to intervene against shocks) and a cyclical instrument (flow of purchases or sales on the market). The closest historical precedent is the post-1990 refill following the Gulf War draws, which proceeded gradually over several years and accompanied rather than dominated the price dynamic of that period.

To understand how this current regime translates into U.S. macro — oil burden ~2.5% well below the critical threshold, core inflation little sensitive to narrow WTI moves — the cluster addresses the question in the current ~2.5% oil burden vs 4-5% threshold and in WTI stability and core inflation.

None of the three readings is exclusive; the three coexist and reinforce each other. The “Chinese demand” reading caps the price from above. The “shale swing” reading stabilizes from below. The “SPR” reading introduces shock asymmetry (weak capacity to draw down to moderate a rise, significant capacity to refill to support a decline). The empirically observed result — $70-85 corridor with compressed volatility — is consistent with the superposition of the three forces. Beyond the cluster, this regime fits within commodities and global macroeconomics and within physical energy markets and geoeconomics which structure the Eco3min analysis of physical markets.

- Since October 2023, WTI in $70-85 corridor with >65% of sessions in that zone and compressed realized volatility 18-28% (vs historical average ~35%)

- Reading 1 — slowed Chinese demand: growth +1.2% per year 2023-2025 versus +4.5% avg 2003-2019, consequence of economic slowdown + EV adoption (>45% new car sales 2024) + heavy industry decline

- Reading 2 — U.S. shale swing producer: Permian break-even $45-55 per Dallas Fed, short-cycle mechanic that dampens in both directions, moderated by capital discipline post-2020

- Reading 3 — SPR at ~370 Mb (52% capacity): weakened draw-down capacity, substantial refill capacity — intervention asymmetry on shocks

Last updated — 12 July 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

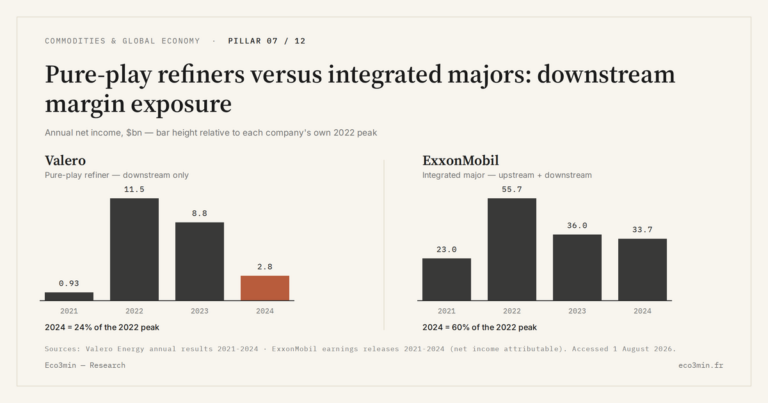

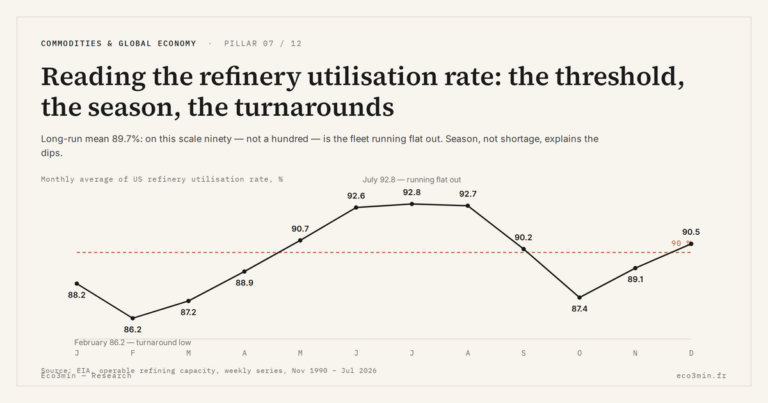

Full pillar →Reading the refinery utilisation rate: the threshold, the season, the turnarounds

A refinery runs full near ninety percent, not a hundred: the last slice of nameplate capacity is a…

IMO 2020: the regulatory shock that rewrote product spreads

An environmental rule on marine sulfur can move a refining spread more than a swing in crude. IMO…

The 2022–2023 refining golden age: anatomy of an episode

In 2022, refined fuel prices climbed faster than crude. That gap, measured by the 3-2-1 crack spread, reached…