Gold and Central Banks: The Record Buying Wave 2022-2026 and the Slow De-Dollarization

Net seller until 2009, the global official sector became a structural gold buyer from 2022 onward, with annual volumes — roughly 1,080 tonnes in 2022 — doubling those of the prior decade.

TL;DR

Net seller until 2009, the global official sector turned structural gold buyer from 2022, absorbing roughly 1,080 tonnes that year, close to a quarter of global demand.

- Three years of rupture: ~1,080 t in 2022, 1,037 t in 2023, ~1,100 t projected for 2024 (World Gold Council), versus ~480 t/year on average over 2010-2021.

- A concentrated core of emerging-market buyers: Turkey peaked at 542 t in 2022, Poland acquired 220 t in 2023, China declared ~316 t from late 2022 to mid-2024.

- The early-2022 freeze of roughly $300 billion in Russian reserves is inferred as the trigger, gold escaping freeze risk because it is held physically in national vaults.

- The dollar's share of COFER reserves fell from 65.7% (1999) to 58.4% (Q1 2026), a slow de-dollarization that gold purchases, excluded from COFER, do not capture.

This buying wave constitutes an underestimated driver in macro analyses of gold prices, and a signal of slow reserve de-dollarization readable in IMF COFER data.

For three decades, central banks represented the blind spot of gold price analysis. Net sellers from the 1990s through the GFC, their return as structural buyers from 2010 was first read as a post-crisis normalization. The near-instantaneous doubling of volumes in 2022 changes the nature of the phenomenon: what was a marginal diversification becomes a structural driver of price formation. To situate this driver within the complete analytical grid, the global monetary signal reading of gold makes it one of the three central channels. This article deploys the application angle: who buys, how much, why, and with what consequences on the international monetary system.

1. From Net Seller to Structural Buyer: the 1990-2024 Sequence in Four Phases

The trajectory of the official sector on the gold market organizes into four clear phases, each bracketed by datable institutional inflections.

Phase 1 (1990-2009): net seller. Over this period, cumulative annual sales by central banks oscillate between 400 and 600 tonnes, with occasional peaks. The most emblematic disposals of the decade are those of the Bank of England, which sells 395 tonnes between 1999 and 2002 — the Brown Bottom sequence, since it coincides with the $252 cyclical minimum of August 1999. The September 1999 Washington Agreements, then the 2004 Central Bank Gold Agreement, cap annual sales by European signatories (primarily eurozone central banks plus Sweden and Switzerland) at 400 tonnes per year on renewable five-year terms. These caps, designed as a market-stabilization measure, in fact mark the last act of the net-seller regime. The wider context: the real-rate sensitivity of gold.

Phase 2 (2010-2021): return to moderate net buying. From 2009-2010, in the immediate wake of the GFC, the official sector flips. Emerging economies — China, Russia, India, Turkey, Kazakhstan primarily — initiate sustained buying programs. Over the decade, average annual net purchases settle around 480 tonnes per the World Gold Council. That level remains within historical norms of the pre-1990 era, and has little visible effect on price formation: the classical two-variable grid (real yields plus dollar) suffices to account for moves observed 2010-2021.

Phase 3 (2022-2024): quantitative break. The sequence shifts brutally from 2022 onward. Annual official-sector purchases double, and the doubling persists for three consecutive years: ~1,080 tonnes in 2022, 1,037 tonnes in 2023, projected ~1,100 tonnes in 2024 (World Gold Council, annual Gold Demand Trends reports). These volumes represent nearly a quarter of annual global gold demand (roughly 4,200 to 4,500 tonnes depending on the year), a proportion without historical precedent over the entire post-Bretton Woods period.

Phase 4 (2025-2026, ongoing): maintenance of volumes at elevated levels, with apparent stabilization around 1,000-1,100 tonnes annually per provisional WGC data for 2025. The question of durability beyond 2026 remains open and is the subject of conflicting analyses.

2. The Record 2022-2024 Volumes: What the WGC Numbers Show

Figures published by the World Gold Council in its quarterly Gold Demand Trends reports and its annual report constitute the reference source for global official flows. The WGC cross-references IMF official declaration data (each signatory central bank publishes its reserves monthly in the International Financial Statistics) with its own field analyses and confidential sources at refineries and bullion banks.

The distinction between declared and inferred purchases is analytically important. Declared purchases correspond to gold reserve variations published to the IMF; they are audit-quality but may omit operations not booked as official reserves (for instance purchases held in distinct sovereign entities, sovereign wealth funds, or off-balance-sheet central bank accounts). The WGC has published since 2020 an estimate of undeclared purchases, ranging by year between 100 and 300 additional annual tonnes versus official declarations. That estimate notably explains some Chinese distortions: the PBoC officially declares relatively moderate reserve variations, while WGC analysts estimate its effective purchases substantially higher.

The breakdown between net buyers and net sellers is also instructive. Over 2022-2024, some central banks remain sellers (Germany, Switzerland marginally, the IMF itself for a few tonnes tied to its sovereign assistance programs), but the global net balance remains massively buyer. The break is therefore not a binary flip but a shift in the weighted average toward buying.

3. Concentrated Buyers: an Identifiable Core and Partial Declarations

Over the 2022-2024 sequence, the main declared buyers concentrate within an identifiable core. Turkey’s CBRT systematically ranks among the top annual buyers, with a 542-tonne peak in 2022 — a historically extreme level explained partly by Turkish private-sector sales repurchased by the central bank. China’s PBoC announces regular monthly purchases between late 2022 and mid-2024, totaling roughly 316 declared tonnes over that window, after a three-year pause in official declarations. India’s RBI acquires regularly between 30 and 80 tonnes per year. Poland’s NBP announced in late 2022 a buying program targeting 100 tonnes per year and effectively acquired 220 tonnes in 2023. Singapore’s MAS made a notable one-off purchase of 76 tonnes in Q1 2023. The Czech National Bank, Uzbekistan’s central bank, the Qatar Central Bank, and Kazakhstan complete the group with more moderate but structurally rising volumes. A complementary angle: the physical pull of gold toward China and India.

This core shares two characteristics. First characteristic: the buyers are predominantly central banks of emerging or semi-emerging economies, with the notable exception of Poland. Second characteristic: their prior gold exposure, measured as a percentage of total reserves, was substantially below historical European levels (typically 5-15% versus 60-70% for France, Italy, Germany, or 75% for the United States). A significant portion of the 2022-2024 purchases can therefore be read as convergence toward historical ratios of large economies, but stated motivations often exceed this technical rebalancing.

4. Motivations: Diversification, Sanctions, Dollar Expectations

Official statements from buying central banks converge on three logics, with weightings varying by country.

First logic: reserve diversification within the context of growing awareness of dollar concentration. This logic is systematically mobilized in official communications because it is technically unimpeachable and politically neutral. It invokes classical portfolio-management principles applied to sovereign reserves: reduced concentration on a single asset, search for low correlation with existing holdings.

Second logic: response to financial sanctions. This logic never appears explicitly in official statements, but it is inferable from time sequences. The case is built out in this analysis of central banks gold accumulation. The post-Crimea annexation sequence in March 2014 marked a first trigger, with an acceleration of Russian (until the 2022 war) and Chinese purchases over 2014-2018. The early-2022 freezing of Russian dollar and euro reserves — roughly $300 billion immobilized in Western central bank accounts — constitutes the phase 3 trigger: it signals to non-Western central banks that reserve assets denominated in adversarial-jurisdiction currencies carry tangible and activatable geopolitical risk, no longer merely theoretical. The arbitrage channel between sanctionable and non-sanctionable assets structurally reorients toward gold, which cannot be frozen since it is held physically in national vaults or in vaults for buyer-country accounts. This analysis is also consistent with the international arbitrage channel between gold and the dollar which then deploys differently from prior cycles.

Third logic: expectations regarding the dollar’s structural role in the international monetary system on decadal horizons. This logic invokes a long-term scenario in which the dollar progressively loses its position as sole reserve currency in favor of a heterogeneous basket. It is more rarely owned publicly by buyers but transpires in some political statements — notably Chinese and Russian — about the necessity of “de-globalizing the yuan” or “developing alternative settlement channels.” Each option is weighed on its own terms in our dollarization-versus-de-dollarization comparison.

5. The Slow De-Dollarization of Reserves: What COFER Shows

The massive gold purchases deploy within a broader macro frame: the slow de-dollarization of global FX reserves. According to IMF COFER (Composition of Official Foreign Exchange Reserves) data, published quarterly with a roughly six-month lag, the dollar share of identified reserves stood at 65.7% in 1999 (first point of the modern series), at 60.5% in 2015, and at 58.4% in Q1 2026 — a cumulative erosion of roughly 7 percentage points over twenty-seven years.

Several analytical caveats apply to this series. First caveat: COFER measures only foreign-currency assets (cash, deposits, sovereign and corporate securities), and explicitly excludes gold. The complete balance dollar plus gold plus other currencies therefore does not read in a single series. Second caveat: composition reported by central banks to the IMF is partial; about 95% of global reserves are allocated-reported, but some significant countries (China partially) do not break down their composition. Third caveat: the 7-point dollar decline has been absorbed by several sources — euro, yuan, other emerging-market currencies, and off-COFER gold. The exact share attributable to gold remains estimative. Further detail: gold measured in March 2026 dollars.

The pace of this de-dollarization remains slow. Over 27 years, 7 points represent roughly 0.26 points per year on average. Even accelerating to 0.5 points annually (the pace observed over 2022-2025), it would take several decades for the dollar to drop below 50%. This inertia is analytically important: it distinguishes effective de-dollarization (slow, observable in the data) from de-dollarization expectations (potentially rapid, embedded in gold prices).

6. What This Wave Means for Price Formation

The analytical contribution of the 2022-2024 buying wave to the gold price reading is threefold.

First contribution: a structural demand floor. An annual flow of 1,000 to 1,100 tonnes represents between 30% and 35% of global mine output (~3,500 t/year per WGC) and nearly a quarter of total demand. This flow mechanically constitutes a demand base that did not exist in prior cycles. That base does not set a particular price, but it reduces the potential downward pressure in case of rising real yields, as the 2022-2024 decorrelation illustrated.

Second contribution: a signal on long-term expectations. Central banks manage their reserves over multi-decadal horizons, with real-value preservation rather than short-term performance objectives. Their massive purchases signal a collective anticipation on the structural trajectory of the dollar and the international monetary system, independent of short rate cycles.

Third contribution: a potential instability trigger if the wave reverses. Should official purchases return to 2010-2021 levels (~480 tonnes annually), the structural demand floor erodes and the price becomes fully exposed again to the classical real yields plus dollar channel. Monitoring the quarterly share of official purchases in total WGC demand is therefore a key indicator to anticipate any regime correction. For the reading of the current regime and its conditional fragility, the $3,000+ regime and the institutional floor proposes a complete interpretive reading.

To situate this wave in the broader macro panorama of effects from a durable strong-dollar regime, the safe-haven myth empirical examination connects with the broader debate on gold’s role under regime shifts. The page on the physical-commodity geoeconomics editorial space aggregates connected analyses.

- Net seller until 2009 (Brown Bottom, 1999 Washington Agreements), the global official sector became a structural buyer from 2010, then a massive buyer from 2022 (~1,080 t in 2022, 1,037 t in 2023, ~1,100 t projected 2024 — World Gold Council).

- The buyer core is concentrated: Turkey, China, India, Poland, Singapore, Czechia, Uzbekistan, Qatar — predominantly central banks of emerging or semi-emerging economies.

- Three logics motivate the purchases: diversification (official), response to sanctions and the 2022 Russian asset freeze (inferred), long-term expectations on the dollar’s role (rarely owned).

- COFER reserve de-dollarization remains slow (58.4% in Q1 2026 vs 65.7% in 1999), but constitutes the macro frame within which the massive gold purchases — invisible in COFER — take place.

Last updated — 12 July 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

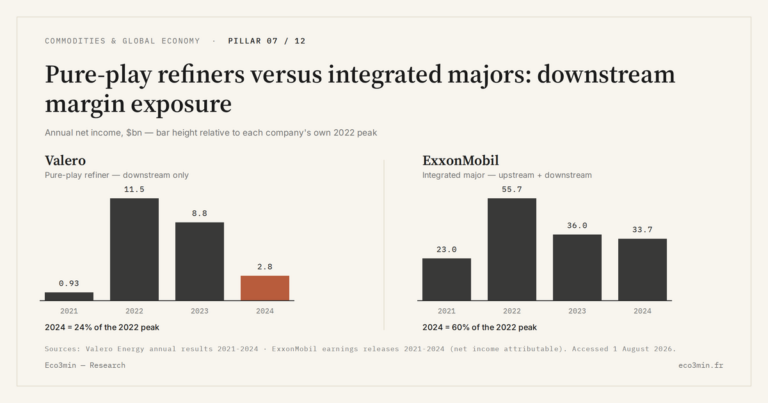

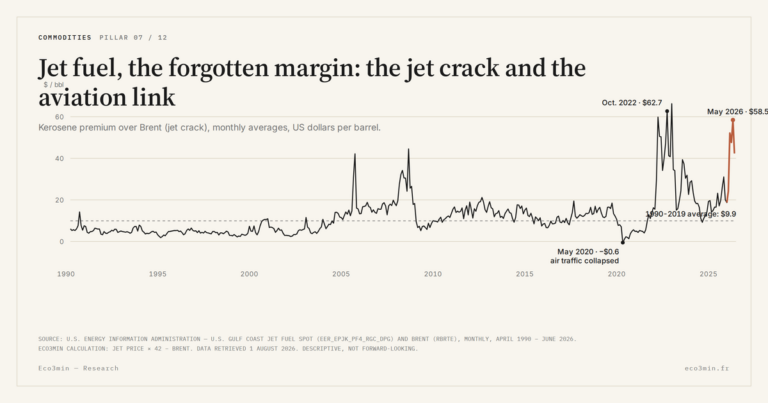

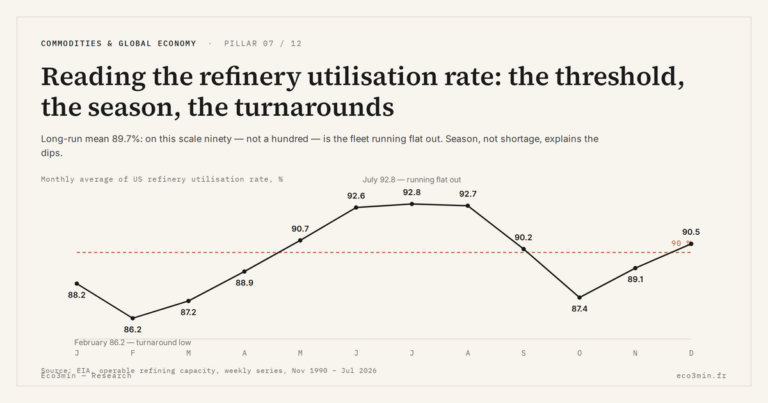

Full pillar →Reading the refinery utilisation rate: the threshold, the season, the turnarounds

A refinery runs full near ninety percent, not a hundred: the last slice of nameplate capacity is a…

IMO 2020: the regulatory shock that rewrote product spreads

An environmental rule on marine sulfur can move a refining spread more than a swing in crude. IMO…

The 2022–2023 refining golden age: anatomy of an episode

In 2022, refined fuel prices climbed faster than crude. That gap, measured by the 3-2-1 crack spread, reached…