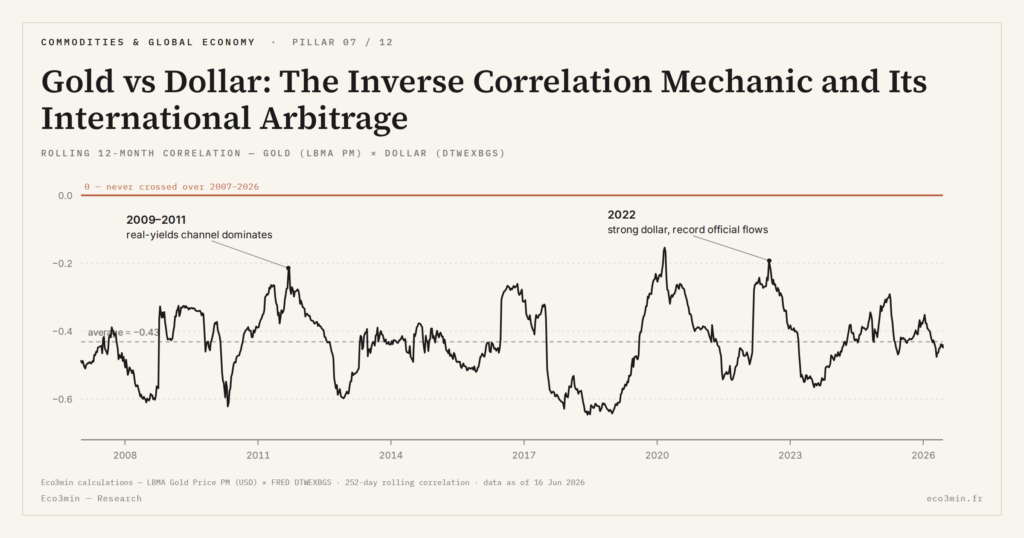

Gold vs Dollar: The Inverse Correlation Mechanic and Its International Arbitrage

The inverse correlation between gold and the dollar is not a statistical coincidence but an international arbitrage mechanic anchored in the fact that gold is quoted in dollars on every global market.

TL;DR

Because gold trades in dollars worldwide, its inverse correlation with the currency is an instantaneous arbitrage equation, not a temporal pattern, and works as a diagnostic, never a predictor.

- Over twenty years, the rolling 12-month correlation between gold and the broad dollar (FRED DTWEXBGS) has run between -0.4 and -0.8, averaging about -0.6, so roughly 36% to 64% of gold's variance traces mechanically to the dollar channel alone.

- The mechanic gets overridden in two documented breaks: in 2008-2011 the correlation fell to -0.2 as 10-year TIPS yields collapsed, and in 2022-2024 it briefly turned positive, with a strong dollar offset by record central-bank buying (~1,080 t in 2022, 1,037 t in 2023).

The correlation is robust over long horizons but admits documented regime breaks that reveal its limits and conditions of validity.

Among the most-cited regularities of the gold market, the inverse correlation with the U.S. dollar occupies a peculiar place. It is systematically invoked in market commentary; it is also frequently overstated as an explanatory variable, or conversely discarded at the first observed exception. The underlying mechanic is in reality simple, robust over long regimes, and instructive precisely in its exceptions. To situate this mechanic within the three-driver reading grid for gold, we begin by clarifying why gold is quoted in dollars and what that fact implies.

1. Why Gold Is Quoted in Dollars: a Post-Bretton Woods Legacy

Before August 15, 1971, the dollar was convertible into gold at a fixed rate of $35 per troy ounce, and all other industrial currencies were tied to the dollar via adjustable exchange rates — the architecture of the 1944 Bretton Woods system. Under that regime, gold did not have a floating market price: it had an administered price, guaranteed by dollar convertibility. The unilateral end of that convertibility by Richard Nixon in August 1971 frees the gold price, which becomes a freely traded asset on markets where the London Bullion Market constitutes the reference. A related read: dollar-priced gold from a euro portfolio.

But that liberalization occurs within an international system where the dollar remains, in practice, the dominant unit of account. Oil has been quoted in dollars since the 1974 Saudi-American agreements. International trade is settled massively in dollars (still about 88% of FX transactions per the BIS Triennial Survey 2022). Official reserves are roughly 58% dollar-denominated (IMF COFER Q1 2026). In that ecosystem, gold — which could in theory have been quoted in several reference currencies — anchors durably to the dollar convention. The London Fix is published in USD/oz; COMEX contracts are denominated in USD; mine production exports, interbank bullion transactions, and the near-totality of derivatives revolve around the same denominator.

It is this single-currency quotation in dollars that opens the international arbitrage mechanic: at any instant, the dollar gold price is what it is, but the gold price in another currency is a function of the exchange rate. And it is this dependence on the exchange rate that produces the observed inverse correlation.

2. The International Arbitrage Mechanic Step by Step

For any buyer outside the dollar zone — for instance an Asian central bank, an Emirati refiner, a Norwegian sovereign fund, or a European retail investor — the local-currency cost of acquiring one ounce of gold equals the dollar price multiplied by the exchange rate. When the dollar depreciates against the local currency, that cost mechanically falls; when the dollar appreciates, it rises.

This mechanic has an immediate consequence on global gold demand. A dollar depreciation supports foreign demand because it lowers the acquisition cost for the majority of marginal market buyers, who are non-American. That strengthened foreign demand pushes the dollar gold price upward until a new equilibrium is reached. Conversely, a dollar appreciation makes gold more expensive for the rest of the world, weakens foreign demand, and exerts downward pressure on the dollar price. The empirical extension shows up in the mapping of gold-demand sources.

Equilibrium is dynamic and continuous: at every instant, bullion-market arbitrageurs — LBMA participating banks, interbank traders, ETF market-makers — adjust their positions to erase any deviation between the dollar gold price and the exchange rate. The inverse correlation is therefore not a fragile statistical regularity: it is an arbitrage equation that holds permanently.

3. The Rolling 12-Month Correlation: What the Data Says Since 1973

Empirically, the rolling 12-month correlation between gold returns and the change in the Trade-Weighted Dollar Index (FRED DTWEXBGS, the broad series preferred over DXY for macro analysis) has oscillated for twenty years between -0.4 and -0.8, averaging around -0.6 (Eco3min calculations on GOLDPMGBD228NLBM × DTWEXBGS series). This range implies that roughly 36% to 64% of gold variance can be mechanically attributed to the dollar over rolling windows — a substantial proportion, but far from exclusive.

Over long regimes, the correlation becomes even sharper. The 1971-1980 cycle sees the DXY move from roughly 120 (1973, index base) to 85 in October 1980, a cumulative depreciation of about 29%, while gold rises from $35 to $850 per ounce — a very clear arbitrage relationship. The 1980-1985 cycle is the mirror: under Volcker tightening (Fed funds at 19% in 1981), the DXY peaks at 164 in February 1985, and gold retreats to $285. The Plaza Accord of September 1985 organizes a coordinated dollar depreciation (DXY from 164 to 95 over the following three years), and gold stabilizes around $400. The 1995-2001 period sees a strong-dollar return under Clinton-Rubin-Greenspan (DXY rising toward 120), gold collapses to $252 in August 1999 — the so-called Brown Bottom.

The 2001-2008 period illustrates the mechanic on a large scale: the DXY drops from 120 to 72 in March 2008, a 40% depreciation, and gold quadruples from $250 to $1,000. Over that window, the rolling 12M correlation reaches -0.85, one of the deepest levels observed since 1973. The 2014-2016 episode delivers the opposite: the divergence of Fed (QE3 exit, first rate hike in December 2015) and ECB (QE entry in March 2015) policy paths drives DXY from 80 to 100, and gold loses 45% from its 2011 peak.

4. Regime Breaks: 2008-2011 and 2022-2024 Explained

The gold-dollar correlation admits two major documented breaks since 2000, and each illuminates the limits of the arbitrage mechanic taken as a single variable.

First break: 2008-2011. During the global financial crisis and the first three Fed QE rounds, gold triples (from $720 to $1,923) while the DXY remains broadly stable between 75 and 85, oscillating around that mean with limited swings. The rolling 12M correlation drops to only -0.2 over 2009-2011. The explanation lies in the temporary dominance of another channel: the collapse of 10-year TIPS yields (from 2.5% in early 2008 to clearly negative levels in 2011 under QE) takes precedence over the dollar channel. Opportunity cost collapses, gold appreciates independently of the dollar trajectory. The international arbitrage mechanic does not disappear — it is dominated by another force.

Second break: 2022-2024, the most recent and most instructive for the current regime. Over that period, the DXY oscillates between 100 and 113 (historically elevated territory, close to the 2002 peak), while gold rises from roughly $1,800 to over $2,000, then crosses $3,000 in March 2025. The rolling 12M correlation turns positive on some windows — an extremely rare phenomenon. The central explanation is the third structural driver: central bank de-dollarization flows and record purchases (~1,080 t in 2022, 1,037 t in 2023, ~1,100 t projected 2024 per World Gold Council) numerically and largely offset the downward pressure exerted by the strong dollar via the classical arbitrage channel.

These two breaks do not invalidate the arbitrage mechanic. They signal that it continues to operate, but can be dominated temporarily by other channels — real yields in 2008-2011, official flows in 2022-2024. This superposition logic characterizes modern analysis of the gold price, and distinguishes a mono-causal reading (“gold rises because the dollar falls”) from a multi-channel reading. For the complementary real-yields channel, which often interacts simultaneously with the dollar channel, the second driver of real yields is treated in a dedicated satellite of this cluster.

5. Reading the Correlation as an Arbitrage Indicator, Never as a Prediction

The correct analytical use of the gold-dollar correlation is not predictive but diagnostic. It does not say “if the dollar falls, gold will rise by X” — a claim that would be false even on short windows because it ignores the other channels. It says, at a given instant T: if a gold price move is observed, one must first verify the dollar channel’s contribution before mobilizing other readings.

Concretely, analysis proceeds in two steps. Step 1: decompose the observed gold move into its “dollar-explained” component (the change in DTWEXBGS over the same window, multiplied by the rolling regression coefficient ~ -0.6) and its unexplained residual. Step 2: examine the residual under other grids — change in TIPS yields, quarterly WGC flows by buyer category, geopolitical events. When the residual is large, one is typically in a regime break (such as 2008-2011 or 2022-2024). When it is small, the classical arbitrage channel suffices.

This analytical discipline has a direct cross-cluster usage: to situate the gold-dollar mechanic in the broader macro context of a durable strong-dollar regime, the dollar’s global reserve role documents the deeper structural dimension of this currency’s position. For the broader physical-commodity-markets ecosystem in which this analysis sits, the geoeconomics of physical commodities sub-pillar aggregates connected analyses.

Reading the gold-dollar correlation as a predictive regularity (“if the dollar falls, gold rises”) is analytically wrong. The correlation is an instantaneous arbitrage equation, not a temporal pattern; it can be dominated by other channels for years, as 2008-2011 (real-yields channel) and 2022-2024 (official-flows channel) have shown. The correct reading is diagnostic: the correlation helps decompose an observed move, never to predict the next one.

Last updated — 12 July 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

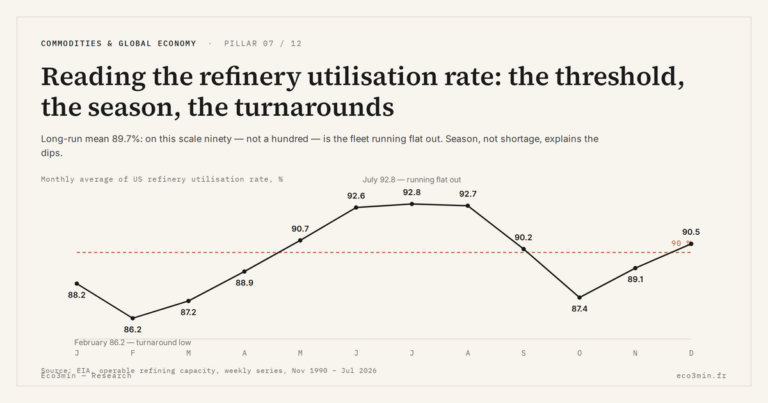

Full pillar →Reading the refinery utilisation rate: the threshold, the season, the turnarounds

A refinery runs full near ninety percent, not a hundred: the last slice of nameplate capacity is a…

IMO 2020: the regulatory shock that rewrote product spreads

An environmental rule on marine sulfur can move a refining spread more than a swing in crude. IMO…

The 2022–2023 refining golden age: anatomy of an episode

In 2022, refined fuel prices climbed faster than crude. That gap, measured by the 3-2-1 crack spread, reached…