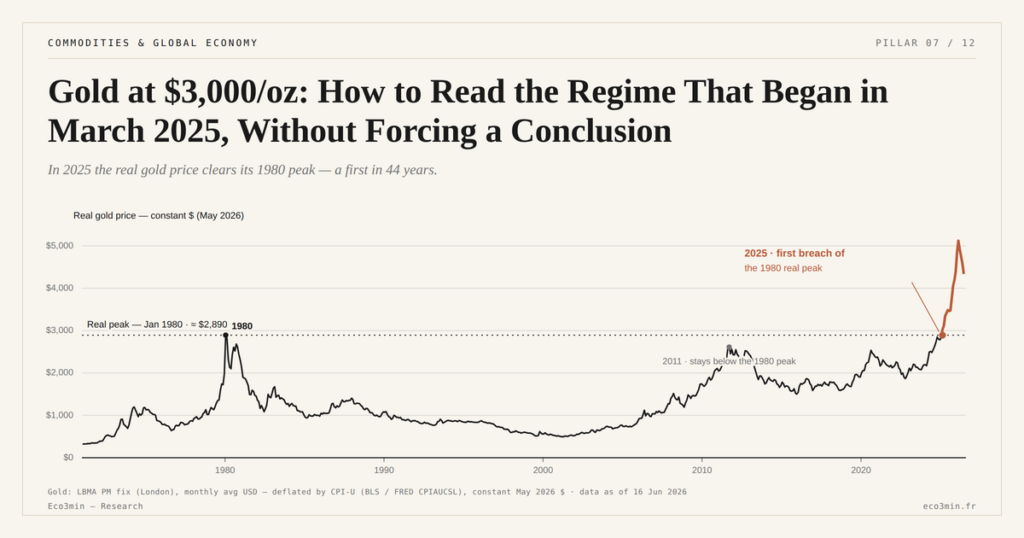

Gold at $3,000/oz: How to Read the Regime That Began in March 2025, Without Forcing a Conclusion

Crossing $3,000 per ounce in March 2025 is a major media inflection point, but analytically it does not reduce to a threshold — it signals the coexistence of three distinct macro readings that no available data can yet arbitrate among.

TL;DR

Gold has held above $3,000 since March 2025, and that level sustains three competing macro readings no available data can yet rank: central-bank demand, de-dollarization bets, perceived debasement.

- Persistence qualifies the regime: over fourteen months above the threshold (mid-May 2026), whereas the 2011 ($1,923) and 2020 ($2,075) peaks each rolled into bear cycles.

- Physical ETFs GLD and IAU turned net-inflowing in H1 2025 after outflows from 2013 to 2024, during which GLD's holdings fell from 1,350 t (2012) to roughly 850 t (end-2024).

- The perceived-debasement reading rests on a US federal deficit near 6% of GDP, debt around 124% of GDP (Q1 2026), and a Fed balance sheet still near $6.8tn versus $4.2tn pre-Covid.

This article proposes a grid for reading this regime without falling into mono-causal projection, and identifies signals to monitor in order to adjust weightings between competing readings.

When a price crosses a round threshold, economic press almost always converts the technical passage into a structuring event. The crossing of $3,000 per ounce in March 2025 did not escape this treatment. But behind the media threshold, the event carries an empirical singularity no prior cycle reproduced: it is the first post-1971 cycle in which the real gold price — that is, adjusted by cumulative CPI inflation — exceeds the historical peak of January 1980. This singularity forces an analytical framework qualitatively distinct from that of prior cycles. To situate it within the complete grid, the cluster’s central hub on gold as a monetary signal makes it the most demanding phase to interpret.

1. March 2025: What Exactly Happened, and Why the Significance Exceeds the Symbolic Threshold

The $3,000 threshold is crossed on the LBMA PM Fix during the first half of March 2025, after several unsuccessful attempts in prior weeks. The exact dynamics of the passage — which session, which volume — matter less than the persistence of the level in subsequent weeks: without return below the threshold through mean reversion, the crossing transitions from noise to regime signal. At the time of writing (mid-May 2026), gold sits substantially above the crossing threshold, and persistence now exceeds fourteen months. Related work: gold as a regime asset.

This persistence qualifies the regime. Unlike prior peaks ($1,923 in September 2011, $2,075 in August 2020), where the top was followed by extended bear cycles, the post-March 2025 sequence shows no major reversal signal on classical technical indicators (long moving averages, momentum, ETF volumes). Net flows on physical ETFs GLD and IAU, which had been massively outflowing between 2013 and 2024 (GLD’s assets under management had dropped from 1,350 tonnes in 2012 to roughly 850 tonnes by end-2024), turn inflowing during the first half of 2025 — a signal of the return of Western financial demand, adding to the official-purchases floor.

2. Nominal Record and Real Record: The Historical Singularity

All prior peaks of the post-1971 cycles were nominal records but never real records once adjusted for cumulative inflation. The $850 nominal peak of January 1980 equated to roughly $3,200 in 2024 dollars under standard conversions on U.S. CPI (BLS, Consumer Price Index for All Urban Consumers). The $1,923 nominal peak of September 2011 equated to roughly $2,670 in 2024 dollars, well below the 1980 real top. Over forty-four years, no bull cycle had allowed gold to surpass its historical real record.

The crossing occurs in 2024, before even the nominal $3,000 crossing: as gold exceeds $2,800 in nominal terms during 2024, it surpasses in parallel the January 1980 real peak according to cumulative CPI calculations. The nominal $3,000 crossing in March 2025 simply consolidates this singularity, documented precisely in the empirical surpassing of the January 1980 real peak.

The analytical significance of this double crossing (nominal and real) differs from that of a simple record. A nominal record reflects cumulative inflation plus factors specific to the gold market. A real record specifically signals that the purchasing power capturable via gold exceeds anything reached since 1971 — that is, throughout the entire modern history of gold as a free asset. This specificity forces qualitatively new macro readings, not reducible to the two-variable grid (real yields plus dollar) historically sufficient.

3. First Reading: Structural Override from Central Bank Buying

The first plausible reading attributes the $3,000+ regime to the persistence of massive central bank purchases. This reading is the most immediately empirical of the three: it builds on measurable data (the quarterly flows published by the World Gold Council) and identifies a direct mechanism (structural demand absorbs a substantial fraction of annual supply, preventing the formation of a classical bear cycle).

Quantitatively, the reading is consistent. An annual flow of 1,000 to 1,100 tonnes represents between 28% and 35% of global mine output (~3,500 tonnes per WGC estimates 2024) and nearly a quarter of total demand. This structural draw modifies the supply-demand balance durably. For the detailed deployment of this analysis, the official-sector buying wave as structural driver documents the 2022-2026 sequence buyer by buyer.

The weakness of this reading is its dependence on the durability of the wave. Should official purchases revert to 2010-2021 levels (~480 tonnes annually), the structural floor erodes. The reading is conditional, and its validity horizon depends on the sovereign decisions of a few identifiable central banks (primarily PBoC, CBRT, RBI, NBP, MAS).

4. Second Reading: Accelerating De-Dollarization Expectations

The second reading places the $3,000+ regime within a trajectory of progressive shifting of the international monetary system toward a multipolar configuration. Under this reading, the gold price captures not effective reserve de-dollarization — which remains slow (58.4% dollar in COFER at Q1 2026 versus 65.7% in 1999, or 0.26 points per year on average) — but the anticipated acceleration of this process by marginal market actors.

This reading is consistent with several parallel observations. First observation: the clear acceleration of the COFER decline since 2022 (from 59% in 2020 to 58.4% in 2026, or roughly 0.11 points per year, faster than the historical average). Second observation: the emergence of bilateral settlement channels in non-dollar currencies — yuan-ruble post-2022 agreements, India-UAE rupee bilateral line from 2023, the BRICS Pay project under discussion since 2023. Third observation: the resilience of gold prices even when TIPS real yields rise (cf. the 2022-2024 empirically documented decorrelation).

The weakness of this reading is the horizon. A shift in the international monetary system unfolds over several decades. Marginal prices can in theory integrate this anticipation at any moment, but this requires assumptions on the convergence of behavior across heterogeneous actors — central banks, sovereign wealth funds, bullion banks, retail — that are not directly observable.

5. Third Reading: Perceived Monetary Debasement

The third reading invokes a less quantifiable but documentable mechanism: the idea that beyond measured CPI, the aggregate of U.S. public liabilities, the fiscal trajectory and anticipated future pressures on the Fed balance sheet degrade the long-run real value of the dollar as a unit of account. Under this reading, the nominal gold price captures not observed inflation but latent inflation — the gap between the current fiscal and monetary trajectory and the trajectory consistent with long-run monetary stability. Related data: Our central-bank assets series.

Several empirical elements feed this reading. The U.S. federal deficit stands around 6% of GDP over 2024-2025 (CBO Congressional Budget Office estimates), historically elevated levels outside recession or war. Federal public debt reaches roughly 124% of GDP at Q1 2026 (US Treasury), a structurally rising trajectory per long-run CBO projections. The Fed balance sheet, after initiating its quantitative tightening (QT) in 2022, remains at roughly $6.8 trillion at mid-2026, substantially above pre-Covid levels ($4.2 trillion in February 2020).

This reading intersects directly with the dismantling of the gold-inflation-hedge myth: precisely because gold does not track observed inflation as a stand-alone variable, it can capture latent inflation not yet measured. The distinction is subtle but analytically decisive. For the empirical foundations of this distinction, the empirical reading of the gold-as-inflation-hedge debate details why the naïve grid fails.

6. Why the Three Readings Coexist and None Lends Itself to Prescription

The central analytical point is that the three readings are not mutually exclusive. They all operate simultaneously, to varying degrees across sub-periods, and the observed price reflects their weighted composition.

The first reading (CB override) is falsifiable on short-to-medium horizons: a return of official flows toward ~480 tonnes annually would clearly invalidate its dominant weight. The second reading (anticipated de-dollarization) is falsifiable only on multi-decadal horizons — it requires watching the COFER trajectory, bilateral agreements, and emerging-market reserve composition over five to ten years. The third reading (perceived debasement) is the least falsifiable in the short term: as long as the U.S. fiscal trajectory does not reverse substantially, latent inflation can be anticipated indefinitely.

The task is therefore not to choose a reading but to hold the three in parallel and observe empirically how their respective weights evolve. This analytical discipline distinguishes a defensible interpretive grid from a projection. To situate the current regime within the full historical sequence, the historical inventory of 1971-2026 cycles documents prior macro regimes and their respective specificities.

7. Signals to Watch in Order to Adjust the Weighting Between Readings

To track the relative evolution of the three readings over time, several empirical indicators are available, each calibrated on one of the grids.

For the CB-override reading: the quarterly share of official purchases in total WGC demand (published in Gold Demand Trends, quarterly). The critical threshold is around 15% of quarterly demand. An abrupt fall below that level, after the 22-25% levels observed in 2022-2024, would signal erosion of the structural floor. For the corresponding cross-read, see the anatomy of global gold demand.

For the anticipated-de-dollarization reading: the quarterly COFER trajectory, in particular the decomposition of the dollar decline among euro, yuan and the “other currencies” category (which includes emerging-market currencies). A sustained acceleration of the “other currencies” share — beyond the historical pace of +0.15 points per year — would signal that effective de-dollarization is catching up with expectations.

For the perceived-debasement reading: the trajectory of the U.S. federal deficit (CBO monthly), the evolution of the U.S. debt-to-GDP ratio, and the differential between 10-year TIPS breakeven inflation (FRED T10YIE) and effective ex-post CPI inflation. A structural widening of this differential would signal that markets are pricing in latent inflation not yet observed.

A transverse indicator also deserves attention: the S&P 500 / Gold ratio (calculated as S&P 500 index divided by the gold price in dollars). This ratio historically oscillates between 1.0 (1980, gold-relative peak) and 6.0 (2000, S&P-relative peak), with a long-run median around 3.5. During May 2026, it sits around 2.0 — a historically low level signaling a rotation favorable to gold against equities. The direction and persistence of this ratio is a synthetic indicator of relative arbitrage between real assets and financial assets. The S&P/Gold ratio signal supports empirical inspection of this indicator.

Monitoring these four indicators — quarterly CB share of total demand, COFER trajectory, breakeven-CPI differential, S&P/Gold ratio — allows dynamic adjustment of the weighting attributed to each reading without resort to operational prescription. The page on the geoeconomics and physical markets editorial silo aggregates connected analyses of physical markets and structural macro signals.

Reading the March 2025 crossing of $3,000 as an eschatological signal — whether as a definitive top heralding a major reversal, or conversely a brakeless bull trajectory — is analytically wrong. The round threshold is technically neutral; what deserves analysis is the combination of the three underlying readings, and the evolution of the four indicators (CB flows, COFER, breakeven-CPI, S&P/Gold ratio) that allow arbitrating between them. Every mono-causal reading of the $3,000+ regime — including the “gold = inflation hedge” reading that resurfaces at every peak — misses the empirical singularity of this phase. Related material: our map of the gold access routes.

Last updated — 12 July 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

Full pillar →Reading the refinery utilisation rate: the threshold, the season, the turnarounds

A refinery runs full near ninety percent, not a hundred: the last slice of nameplate capacity is a…

IMO 2020: the regulatory shock that rewrote product spreads

An environmental rule on marine sulfur can move a refining spread more than a swing in crude. IMO…

The 2022–2023 refining golden age: anatomy of an episode

In 2022, refined fuel prices climbed faster than crude. That gap, measured by the 3-2-1 crack spread, reached…