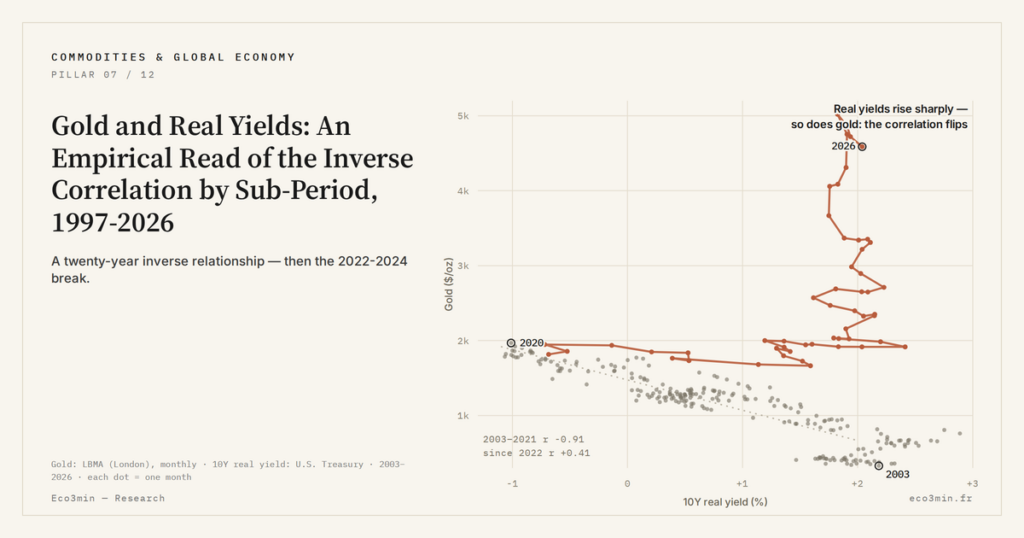

Gold and Real Yields: An Empirical Read of the Inverse Correlation by Sub-Period, 1997-2026

The inverse correlation between gold and the 10-year TIPS yield is empirically documented over nearly thirty years, but it has never been a stable coefficient: it deforms and breaks according to macro regimes.

TL;DR

Gold's usually inverse tie to ten-year real yields broke for three years running: yields climbed 3.5 points after 2020 while gold rose, flipping the correlation positive on some quarters.

- FRED's DFII10 series gives the real yield on 10-year TIPS, indexed to CPI-U since January 1997; across the founding 1997-2007 decade its rolling 12-month correlation with gold held between -0.5 and -0.85 (about -0.72 on average).

- Through 2008-2011, DFII10 fell from +2.5% to -0.5% across three QE rounds while gold ran from $720 to $1,923, and the correlation reached -0.90 over 2010-2011, the opportunity-cost channel alone accounting for the entire move.

- The 2022-2024 decorrelation held for three years, with a positive correlation appearing under 5% of the time since 1997 and an unexplained residual of roughly +$800 to +$1,000, pointing to a non-real-yields channel driving the price.

- Since late 2024, DFII10 has eased to around 1.70% (mid-May 2026) and the correlation has settled near -0.4, weaker than the 1997-2020 average of -0.72, as gold crossed $3,000 (March 2025) over a floor held by ~1,100 t/year of official buying (WGC).

This article does not restate the theoretical opportunity-cost mechanic — covered elsewhere. It deploys a strictly empirical reading, sub-period by sub-period, of data available since the 1997 TIPS launch.

The relationship between gold prices and the real yield on 10-year Treasury Inflation-Protected Securities is among the most cited in market literature — sometimes to the point of masking its real empirical variability. The rolling correlation coefficient is not a constant. Over the window available since the TIPS launch in January 1997, six sub-periods of distinct statistical behavior are clearly identifiable, each illuminated by its own macro reading. This logic is brought out in the critical reading of linkers against inflation. For the theoretical opportunity-cost mechanic underlying the relationship — why a non-yielding asset depreciates when the alternative real yield rises — the generic framework is covered separately. The present article distinguishes itself by angle: here, we read regimes, not theory.

1. 10-Year TIPS (DFII10): What the Series Actually Measures

Before any empirical reading, the perimeter of the DFII10 series deserves to be stated without ambiguity. Launched in January 1997 by the U.S. Treasury Department, Treasury Inflation-Protected Securities are bonds whose principal is adjusted daily to BLS-published CPI-U inflation. The published yield — the FRED DFII10 series — is the market yield on adjusted principal, hence an expected real yield by construction. The 10-year breakeven, calculated as the spread between nominal 10Y Treasury (FRED DGS10) and DFII10, gives by construction the market-expected average inflation over the 10-year horizon. Underlying data: the 10-year breakeven record.

This series is available daily since January 2, 2003 in its most continuous form; the earliest years 1997-2002 had lower liquidity and sometimes patchy coverage. For precision macro analysis, most reliable series begin around 2003. Beyond the technical limitations, DFII10 properly reflects the real opportunity cost of a risk-free bond investment over the 10-year horizon, making it the reference proxy for gold-real-yields analysis. A related question: why real yields matter more than nominal.

2. 1997-2007: Calibrating the Correlation, the Founding Decade

Over the first continuous-quotation decade, the gold-real-yields relationship installs itself clearly. The DFII10 yield oscillates between 1.5% and 3.5%, with a peak at 3.1% in June 2000. The gold price recovers progressively from the $252 floor (Brown Bottom, August 1999) toward roughly $700 by mid-2007. The rolling 12-month correlation on GOLDPMGBD228NLBM × DFII10 oscillates between -0.5 and -0.85, averaging around -0.72 (Eco3min calculations). This strong statistical range reflects a working arbitrage mechanic: when DFII10 rises, gold stalls or retreats; when DFII10 falls, gold appreciates. In depth: the structure of gold demand from ETFs to physical bars.

The period is also characterized by the absence of major monetary stress — the Greenspan-led Fed operates through micro-adjustments on Fed Funds, CPI inflation stays contained (around 2-3%), the dollar weakens slowly from 2002 with the Iraq invasion and the widening twin deficits. In this relatively calm environment, the real-yields channel dominates without significant interference. This decade serves as the implicit reference for every subsequent assessment of “is the correlation still there?” produced during later breaks.

3. 2008-2011: GFC and Three QE Rounds, the Correlation at Its Extreme

The global financial crisis produces the most spectacular sequence of the empirical TIPS history. Between January 2008 and August 2011, the DFII10 yield plunges from +2.5% to -0.5% — a three-point compression in under four years, under the combined effect of flight-to-quality, three Fed QE rounds (QE1 November 2008, QE2 November 2010, Operation Twist September 2011, QE3 in September 2012) and the brutal collapse of long-run inflation expectations.

Gold prices trace the mirror trajectory: $720 in November 2008 (post-Lehman floor), then $1,923 in September 2011 (nominal historical peak of this sequence). The rolling 12M correlation reaches -0.90 over the 2010-2011 window, one of the deepest levels ever observed on this series. For this period, the single-channel grid — real opportunity cost — suffices: the totality of the gold move is explained by the DFII10 trajectory, without need to mobilize other readings. Also relevant: the opportunity cost of holding gold.

The September 2011 peak closely coincides with the first S&P downgrade of the U.S. sovereign AAA (August 5, 2011) and the entry into the eurozone sovereign debt crisis. This concomitance provides a robustness test: even in the most acute systemic stress peak since the GFC, the real-yields channel remains analytically sufficient to account for the observed price. The “systemic safe haven” factors invoked in contemporary press are then largely redundant with the real-yields channel itself.

4. 2011-2020: Fed Normalization and a Stable but Weakened Correlation

The 2011-2020 period sees a consolidation of the relationship at an average correlation level around -0.65, weaker than the prior decade. Three main sub-windows succeed each other.

2011-2015: classical mean-reversion phase. The taper tantrum (May 2013 QE3 tapering announcement), the end of QE3 in October 2014, and the first Fed Funds hike in December 2015 organize a gradual DFII10 climb from -0.5% to +0.7%. Gold retreats in parallel from $1,923 to $1,050 (December 2015), a 45% loss. The rolling 12M correlation stays around -0.75 over this window.

2016-2019: macro-stable zone. The Fed delivers nine hikes between December 2015 and December 2018, DFII10 oscillates between 0.3% and 1.0%, gold stabilizes within a $1,100-$1,350 range. The rolling 12M correlation weakens to around -0.55 — still negative, but with wider dispersion. This phase signals that under “calm” monetary regimes, the real-yields channel loses some explanatory power, perhaps in favor of idiosyncratic factors (speculative ETF flows, trade-policy expectations under the Trump administration, etc.).

2020: Covid shock. In March 2020, the Fed deploys unlimited QE, brings Fed Funds to zero, and floods the system with liquidity. DFII10 plunges to -1.06% in August 2020 — the lowest historical level ever recorded on this series. Gold crosses $2,000 for the first time in August 2020 (peak at $2,075). The correlation restores brutally to -0.87 over the 2020 window. The real-yields channel dominates without contest.

5. 2022-2024: The Major Empirical Break and What It Reveals

The 2022-2024 period constitutes the most instructive break in the empirical TIPS history. Over this three-year window, the DFII10 yield performs a climb of unprecedented amplitude: from -1.06% in August 2020 to +2.50% in October 2023 — a 3.5-point variation in roughly three years, comparable in magnitude to the Volcker tightening of the 1980s on the real component.

Under the classical grid calibrated on 1997-2020, this real-yields climb should have triggered a gold price collapse of around 35 to 50%, implying a return toward $1,100-$1,200. Yet gold does the opposite: it progresses from $1,800 (March 2022) to $2,080 (end-2023), a 12% gain while opportunity cost climbs historically. The rolling 12M correlation turns positive on several quarterly windows between mid-2022 and early 2024 — a historically extremely rare phenomenon, observed less than 5% of the time since 1997.

This decorrelation is not transient statistical noise. It lasts three years, and its amplitude (residual unexplained by DFII10 of the order of +$800 to +$1,000 depending on the window) exceeds by several standard deviations the normal variation bands of the relationship. The reading that imposes itself is that an alternative channel — different from real yields — numerically dominates price formation over this period. Three plausible readings coexist to explain this channel, of which the first — structural override from central bank buying — is treated specifically in the central bank channel and the 2022-2024 decorrelation. The other two — de-dollarization expectations and perceived monetary debasement — are synthesized in the analytical framework for gold as a monetary signal of this cluster.

6. 2024-2026: Partial Return to the Grid Under Central Bank Override

From late 2024, the situation evolves. The DFII10 yield gradually retreats as markets anticipate forthcoming Fed cuts: it settles around 1.70% by mid-May 2026, down 80 basis points from the October 2023 peak. Over the same window, gold crosses $3,000 in March 2025 and continues to climb. The rolling 12M correlation moves back into negative territory but around -0.4 — substantially weaker than the 1997-2020 historical average (-0.72).

This partial restoration suggests that the real-yields channel operates again, but with a reduced relative weight. The structural buying flow from central banks (~1,100 t/year per WGC) remains active and maintains an independent price floor. For the attentive reader, this configuration imposes a two-channel simultaneous reading grid: real yields for the short-to-medium cyclical component, central banks for the structural floor. The correct superposition of these two readings is the condition to interpret the $3,000+ regime and its empirical rupture without falling into mono-causal projection.

7. A Live Mechanic, Never a Stable Coefficient

The central lesson of this empirical reading sub-period by sub-period is that the gold-real-yields correlation is neither a stable regularity nor a fiction. It is a live mechanic whose relative weight varies with dominant macro regimes. When the real-yields channel dominates alone (1997-2007, 2008-2011, 2020), it accounts for nearly all of the price. When another major channel activates — official buying in 2022-2024, perhaps soon de-dollarization expectations — the real-yields channel persists but becomes one channel among several, and the rolling correlation weakens or temporarily inverts. Directly related: the tax bill behind exiting gold.

To situate this empirical reading in the broader macro panorama, the complete inflation guide documents the conceptual framework in which breakeven expectations and the TIPS-CPI relationship sit. The CPI-adjusted gold price dataset supports the empirical inspection of the real-terms claims made here. The page on the broader physical commodities ecosystem aggregates connected analyses on commodities and structural macro signals.

- The rolling 12M correlation between gold and TIPS real yields has oscillated since 1997 between -0.2 and -0.9; its historical average is around -0.7, but it has never been a stable coefficient.

- Four sub-periods confirm the classical real-yields-channel grid (1997-2007, 2008-2011, 2011-2015, 2020) with correlations from -0.55 to -0.90.

- The 2022-2024 break produces positive rolling correlations over some quarterly windows — a phenomenon observed less than 5% of the time on the full series; its amplitude exceeds several standard deviations of normal variation.

- The current regime (2024-2026) is a two-channel simultaneous configuration: real yields for the cyclical component, official central bank buying for the structural floor. Mono-causal reading is wrong by construction.

Last updated — 12 July 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

Full pillar →Reading the refinery utilisation rate: the threshold, the season, the turnarounds

A refinery runs full near ninety percent, not a hundred: the last slice of nameplate capacity is a…

IMO 2020: the regulatory shock that rewrote product spreads

An environmental rule on marine sulfur can move a refining spread more than a swing in crude. IMO…

The 2022–2023 refining golden age: anatomy of an episode

In 2022, refined fuel prices climbed faster than crude. That gap, measured by the 3-2-1 crack spread, reached…