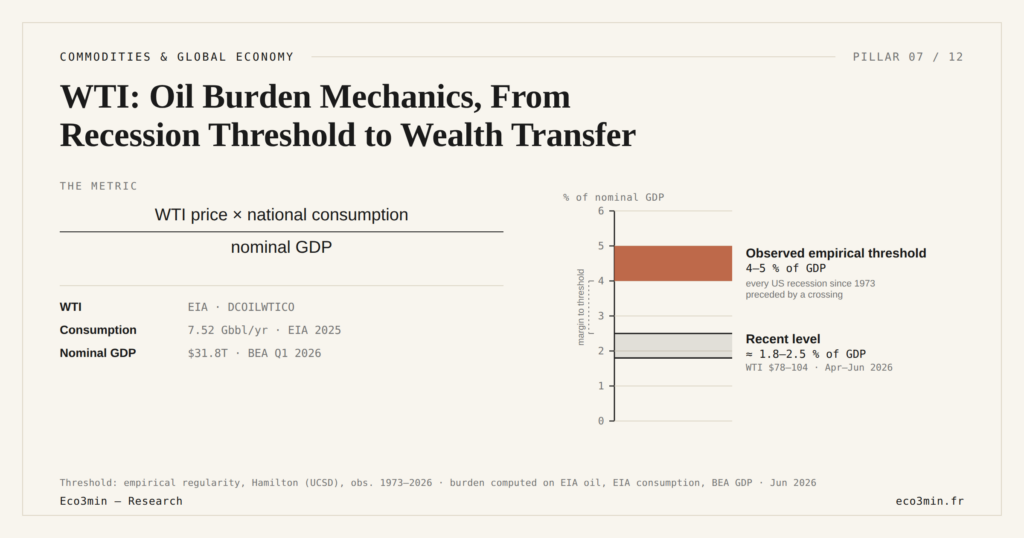

WTI: Oil Burden Mechanics, From Recession Threshold to Wealth Transfer

The oil burden measures oil’s weight in the economy: WTI price × national consumption / nominal GDP. Formalized by James Hamilton from 1983 onwards, the metric indicates that above 4-5% of GDP, three transmission channels produce a cumulative dynamic that slides into recession.

TL;DR

Since the U.S. turned net oil exporter in 2019, the recession-signaling oil burden works asymmetrically: it still bites households through budgets while the wealth-transfer channel flows inward to U.S. producers.

- The metric, formalized by James Hamilton (UCSD) from 1983, sits near 2.5% of GDP in May 2026 (WTI around $75 times 7.5 billion barrels divided by $28.5 trillion GDP), so reaching 4% would need WTI durably above $115-120.

- Lifting the burden toward the 4% zone would require three joint conditions: a durable price breakout, no offsetting shale supply response, and U.S. consumption that fails to adjust through efficiency or substitution.

This piece exposes the mechanics in three channels. The case-by-case empirical audit of each recession since 1970 is addressed in a separate dedicated study; here, the angle is transmission, not the episode.

1. The Metric: Definition and Empirical Threshold

The oil burden is calculated simply: crude price × national consumption in barrels / nominal GDP. For the United States, Eco3min calculations use FRED DCOILWTICO for the price, EIA data for consumption (about 7.5 billion barrels per year in 2025), and BEA nominal GDP. The formula comes from a series of papers by James Hamilton (UCSD) initiated in 1983; it has evolved little over four decades because its statistical robustness across five decades makes it a reference signal in U.S. empirical macroeconomics. For context: the implicit arbitrage between store of value and energy input.

Per Eco3min calculations, every U.S. recession since 1973 has been preceded by an oil burden equal to or above 4% of GDP. The list of the seven recessions concerned: 1973-1975, 1980, 1981-1982, 1990-1991, 2001, 2008-2009, 2020. For the case-by-case empirical detail — burden magnitude, threshold-crossing duration, associated output gap — Eco3min has published an in-depth study, the empirical oil-burden study by recession (chronological audit with datavisualizations).

The 4-5% threshold is not inscribed in economic theory in the strict sense. It is an empirical regularity observed in the data — not a structural law. Its robustness comes from cumulative observation, not from a model derived from microeconomic axioms. This makes it a practical signal but one that must be read with awareness of its empirical nature: crossing the threshold does not mechanically guarantee a recession, and a recession can theoretically occur without a prior crossing. Across five decades, however, the correlation is robust enough to serve as an operational reference.

The current level (May 2026) is approximately 2.5% of GDP per the Eco3min calculation (WTI averaging around $75 × 7.5 billion barrels / $28.5 trillion nominal GDP). On a nearby slope: WTI Explained: Meaning, Calculation, and Cushing Spot Benchmark. This is well below the critical threshold. For the burden to reach 4%, at constant GDP and consumption, WTI would need to be durably above $115-120 — a level out of reach in the current stabilization regime. Worth reading alongside: our compared read of uranium and hydrocarbons.

2. Three Mechanical Transmission Channels

The mechanism by which a high oil burden slides into recession operates through three distinct channels that add up.

First channel: wealth transfer to producers. When the price rises, net oil exporters — OPEC+ historically, the United States since 2019 — receive increased revenues. But their marginal propensity to consume or invest in the global economy is lower than that of net importers. A significant share of the transfer is saved as foreign exchange reserves, recycled into international financial assets (the famous petrodollars of the 1970s), or invested in sovereign wealth funds with long horizons. Quantitatively, BIS and IMF figures over 1973-2014 estimate the marginal savings rate of OPEC exporters reaches 50-70% of additional oil revenues during peak episodes — versus 5-10% for the marginal propensity to consume of equivalent U.S. households. This allocation friction produces a net compression of global aggregate demand, particularly pronounced when prices exceed $80-100. A related read: WTI 2024-2026: The $70-85 Stabilization Regime and Volatility Compression.

Second channel: terms-of-trade distortion. A net oil-importing country sees its trade balance mechanically deteriorate when the price rises. The macroeconomic counterpart is a compression of aggregate domestic purchasing power. For European economies and Japan, dependent on energy imports at 90-95%, this channel is particularly strong: a 30% WTI shock typically translates into a 0.5 to 1 point of GDP deterioration in the European trade deficit per European Commission estimates. For the United States, which became a net exporter in 2019, this channel is partially neutralized at the aggregate level — but remains active regionally, with producing states (Texas, North Dakota, New Mexico) gaining at the expense of net importing states (East Coast, West Coast, Midwest outside producers).

Third channel: contraction of household discretionary demand. Energy’s share in U.S. household budgets per the BLS Consumer Expenditure Survey went from 4% in 1970 to a peak of 9% in 1980, then fell back to 3-4% in the 2000s and rose again to 5-6% during recent peaks. When energy devours a growing share of the budget, households compress discretionary spending — restaurants, leisure, durable goods — which are precisely the most cyclical components of GDP. This discretionary contraction amplifies the slowdown induced by the first two channels.

The three channels do not act with the same intensity depending on context. In a net-importing economy, channel 2 dominates; in a net-exporting economy, channel 1 partially inverts (the country benefits from the transfer) and channel 3 remains structurally active on households. For the contemporary macro reading of the United States as a net exporter, the oil burden retains predictive power via channel 3, attenuated by the partial neutralization of channels 1 and 2.

3. Why 4-5% and Not Another Threshold

The 4-5% threshold is not derived from a theoretical model but from empirical observation across five decades. Three structural mechanisms explain why economies tip in this zone.

First, the threshold corresponds approximately to the share of energy in household budgets that becomes prohibitive for discretionary spending. At 4-5% of GDP devoted to oil, plus the share of total energy (gas, electricity), households typically reach 8-10% of disposable income devoted to energy. Beyond, discretionary compression becomes brutal and amplifies the other channels.

Second, the threshold historically corresponds to the moment when inflation expectations begin to de-anchor. The oil shocks of 1973-1974 and 1979-1980 produced double-digit inflation precisely because pass-through combined with expectations that were not yet anchored by credible monetary policy — a phenomenon Hamilton and Kilian have empirically documented. Post-Volcker, the anchoring is better, but the 4% threshold remains the stable empirical observation.

Third, the threshold corresponds to the practical limits of short-term energy substitution. An economy can shift toward other energy sources (gas, electricity, renewables) but these substitutions take years and require capital. On a quarterly horizon, substitution is limited; the economy bears the shock in proportion to its oil dependence, and it is this short-term inelasticity that produces the recession dynamic when the burden crosses the threshold. In depth: the constraint side of physical commodities.

A fourth, more recent dimension is worth flagging. Since the shale revolution and the U.S. shift to net exporter status, the empirical threshold may behave asymmetrically across countries. For traditional net importers (Europe, Japan, India), the 4-5% threshold retains the historical mechanical force across all three channels. For the United States, the threshold remains operative through channel 3 (household discretionary compression) but the wealth-transfer channel partially reverses — when WTI rises, U.S. producers receive the transfer rather than send it abroad. This empirical complication does not invalidate the threshold; it complicates the international comparison, since the same WTI price now produces a different distributional pattern in the U.S. compared with what it produced before 2019. Empirical work on whether the threshold is shifting upward for the U.S. remains active in the academic literature.

For the historical grid of the seven shocks that produced these crossings, the cluster addresses the question in the oil shocks and historical oil burden. For the pass-through inflation that intersects with the oil burden, the cluster details the mechanics in inflation and oil pass-through.

4. Reading the Current Burden Without Overinterpreting

The current level ~2.5% of GDP signals no recessionary dynamic from the oil channel. This is both reassuring and insufficient for a complete macro reading: a low burden does not exclude a recession produced by other channels (monetary tightening, financial imbalance, external contraction), as illustrated by the COVID 2020 recession which had no prior oil cause.

Concretely, three conditions would need to combine for the burden to approach the critical zone in the current regime. First, a durable WTI breakout above $115-120, requiring either a major supply shock (Middle East large-scale conflict affecting Hormuz throughput, Russia escalation cutting off remaining Russian exports) or a structural demand acceleration (Chinese reflation, sustained global growth surprise to the upside). Second, an absence of compensating shale supply response: the U.S. shale’s short-cycle nature historically caps sustained price overshoots, so the breakout would need to coincide with either shale capacity constraints (drilling productivity declines, capital discipline retention) or accelerated demand outpacing capacity. Third, a U.S. consumption that does not adjust downward via efficiency gains or behavioral substitution. None of these conditions is implausible in isolation; their joint occurrence is what would lift the burden from ~2.5% to the 4% threshold zone.

The analytical reading therefore consists of using the burden as one composite barometer among others, not as a single indicator. For the broader role of WTI in U.S. macro, the reference is the cluster’s WTI as upstream macro signal. For the public-facing summary in English, the Eco3min FAQ on oil and recessions covers the principal episodes in synthesis. For the in-depth recession-by-recession empirical audit, the canonical reference remains the chronological burden audit on Eco3min — the present article positions the transmission mechanics, the chronological study positions the case-by-case empirical record.

Beyond the cluster, the burden reading fits within commodity regimes and global economy and within resource geoeconomics which structures the Eco3min analysis of physical energy markets.

- Oil burden = WTI price × national consumption / nominal GDP — metric formalized by James Hamilton (UCSD) from 1983, stable for four decades

- Observed empirical threshold 4-5% of GDP: every U.S. recession since 1973 has been preceded by a crossing (1973-75, 1980, 1981-82, 1990-91, 2001, 2008-09, 2020)

- Three mechanical channels: wealth transfer to producers, terms-of-trade distortion, contraction of household discretionary demand

- Current level ~2.5% of GDP (May 2026) — well below the threshold; for the burden to reach 4%, WTI would need to be durably above $115-120

Last updated — 12 July 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

Full pillar →Reading the refinery utilisation rate: the threshold, the season, the turnarounds

A refinery runs full near ninety percent, not a hundred: the last slice of nameplate capacity is a…

IMO 2020: the regulatory shock that rewrote product spreads

An environmental rule on marine sulfur can move a refining spread more than a swing in crude. IMO…

The 2022–2023 refining golden age: anatomy of an episode

In 2022, refined fuel prices climbed faster than crude. That gap, measured by the 3-2-1 crack spread, reached…