WTI: Oil Shocks 1973-2026 and the Major Energy Crises

Since 1973, WTI has traversed seven major shocks. Each combines in variable doses three ingredients — physical supply constraint, structural demand pull, financial stress — whose identification enables reading the nature of the shock rather than its magnitude alone.

TL;DR

Reading WTI's seven shocks since 1973 turns on the dosage of supply, demand, and financial stress; the nominal 2008 peak of $145.29 even sits below 1980 once adjusted for inflation.

- The 1990 Gulf War shows magnitude tracks perceived duration as much as volume: roughly 4.3 Mb/d of Iraqi-Kuwaiti exports vanished, WTI ran from about $17 to $40, then fell below $20 by March 1991 once Desert Storm resolved it.

- The March 2022 Ukraine peak of $123.70 stayed below 2008's $145 as U.S. shale added swing capacity and the December 2022 G7 cap kept Russian Urals flowing at $60.

This piece maps the seven shocks. The empirical audit of the oil burden threshold specific to each recession is addressed elsewhere; here, the focus is the shocks themselves — their triggers, magnitudes, and analytical classification.

1. The Grid of Seven Shocks: Three Combinatorial Ingredients

Per FRED data (DCOILWTICO daily since 1986, WTISPLC monthly since 1946), seven episodes stand out as major shocks on WTI or its contemporary equivalent: the 1973 Arab embargo, the 1979 Iranian Revolution, the 1990 Gulf War, the 2003-2008 China super-cycle, the 2011 Arab Spring, the April 2020 COVID shock, and the March 2022 Russian invasion of Ukraine. These seven episodes are not the entirety of WTI moves over the period, but they concentrate its extreme variations — typically more than 50% movement over less than 12 months, either up or down. Related analysis: The chronology of gold priced in barrels of crude.

The analytical grid mobilizes three ingredients that interact. The first is physical supply constraint: sanctions, embargoes, conflicts affecting production capacity or transport routes. The second is structural demand pull: rapid industrialization of a major consumer country, post-crisis recovery, strategic stockpiling. The third is financial stress: speculative positioning, dollar movements, flight to commodities as an asset class in inflationary periods. No major shock is mono-causal; all combine the three ingredients in variable doses. On the same theme: commodities and the headline-core gap.

Identifying the dosage matters for the macro reading. A predominantly supply shock (1973) calls for a different response than a predominantly demand shock (2008) or a predominantly financial shock (post-2009 normalization). For the WTI as composite macro indicator, the nature of the shock conditions the analytical function mobilized (oil burden, pass-through inflation, geopolitical premium).

A methodological remark. The magnitudes cited below mix nominal and real prices depending on the academic reference sources. For the most rigorous inter-episode comparisons, using the CPI-adjusted real price series is recommended — it reveals, for instance, that the nominal July 2008 peak at $145 is below the 1980 peak in real terms once adjusted for cumulative inflation. Eco3min tracks the CPI-adjusted series via the real WTI series CPI-adjusted on Eco3min. The figures below are nominal prices as observed.

2. The Supply Shocks of the Twentieth Century (1973, 1979, 1990)

The first modern oil shock is the Arab embargo of October 1973. On October 17, 1973, the Arab member countries of OPEC (OAPEC) decided on an embargo against countries supporting Israel during the Yom Kippur War. Per EIA data on the average U.S. crude import price, the price goes from about $3 per barrel in September 1973 to $12 in March 1974 — quadrupled in six months. This episode is almost pure supply: global demand does not change significantly, but physical access to Middle Eastern crude is voluntarily restricted. The macro consequence is the 1974-1975 stagflation: U.S. recession and double-digit inflation, first empirical demonstration of the pass-through channel. Eco3min covers it in detail in the chronology of the 1973 oil shock.

The second major shock is the Iranian Revolution of 1979. Between January 1978 and February 1979, the Shah regime collapses and Iranian production collapses with it, going from 5.5 to less than 2 million barrels per day per EIA data. The Iran-Iraq War starting in September 1980 amplifies the shock. The average crude price goes from about $14 in early 1979 to $39 in November 1980 — tripled in less than two years. As in 1973, it is a supply-dominated shock, with a regional geopolitical dimension that extends the effect. The 1980-1982 U.S. recession and inflation above 14% in 1980 confirm the pass-through and oil burden grid. In the same vein: the uranium-fossil-fuel comparison.

The third supply shock of the twentieth century is the Gulf War of 1990-1991. On August 2, 1990, Iraq invades Kuwait, and the combined exports of these two countries (about 4.3 million barrels per day per EIA) are withdrawn from the market by UN sanctions. WTI goes from about $17 in July 1990 to $40 in October — a short spike of limited magnitude compared to 1973 and 1979. The speed of the military coalition and the launch of Operation Desert Storm in January 1991 resolve the shock within a few months: WTI returns below $20 in March 1991. This episode demonstrates that the magnitude of a supply shock depends not only on the volume withdrawn but on the perceived duration of the disruption.

For each of these three episodes, the U.S. oil burden crossed the critical threshold of 4-5% of GDP, contributing to preceding or deepening the U.S. recessions of 1973-1975, 1980-1982, and 1990-1991. The cluster’s oil burden and recession threshold details the quantitative mechanics; for the broader case-by-case empirical panorama, Eco3min has published an empirical oil-burden study by shock, and the public-facing summary covers these episodes in oil spikes before recessions.

3. The Super-Cycle and the Arab Spring (2003-2008, 2011)

The fourth shock — also the only one truly dominated by demand in the grid of seven — is the 2003-2008 super-cycle. Over five years, WTI goes from about $30 in early 2003 to a historic peak of $145.29 on July 3, 2008 (FRED DCOILWTICO). The dynamic is unprecedented: accelerated Chinese industrialization post-WTO (China joins the organization in December 2001) massively pulls global oil demand. Per EIA figures, Chinese demand goes from 4.8 Mb/d in 2000 to 7.7 Mb/d in 2008. This structural progression intersects with an OPEC+ supply slow to invest and with a weak dollar (the DXY index falls from 121 in 2002 to 71 in July 2008), which mechanically amplifies the dollar-denominated crude rise.

The financial dimension of the super-cycle is significant. Institutional investor flows into commodities as an asset class (the S&P GSCI and BCOM indices experience massive inflows over 2003-2008) add a layer of non-physical demand that amplifies the move. When the financial crisis erupts in 2008 (Lehman Brothers, September 2008), WTI collapses from $145 to $33 in less than five months — a fall confirming that the rise contained a superimposed financial component that violently reversed. This episode is the clearest illustration of a combined structural demand + financial stress shock. These shocks take their place among the regime-defining crises gathered in our macro-financial crises timeline.

The fifth shock is the Arab Spring of 2011. Following the uprisings in Tunisia, Egypt, Libya, and Syria in early 2011, WTI rises from $85 in January 2011 to $113 in May 2011. Libya temporarily loses nearly all of its production (1.6 Mb/d withdrawn from the market between February and August 2011 per EIA). But the macro context is very different from earlier shocks: the global economy is still recovering post-GFC, stocks are progressively rebuilding, and the U.S. Strategic Petroleum Reserve releases 30 million barrels in June 2011 (coordinated IEA program). WTI returns to around $80-90 over the 2011-2014 period, without triggering a U.S. recession — the oil burden remains below the 4% threshold.

The 2011-2014 period also sees the development of the WTI-Brent structural differential addressed elsewhere in the cluster, as the U.S. shale boom creates a local surplus that decouples WTI from Brent. These deep dynamics durably modify the macro reading of the U.S. barrel from 2015 onwards. For the inflation transmission mechanics of these shocks, the cluster’s inflationary pass-through of shocks details pass-through elasticity by regime.

4. The Era of Crossed Shocks (COVID 2020, Ukraine 2022)

The sixth shock — the April 2020 COVID shock — is unprecedented in the grid of seven. On April 20, 2020, the WTI front-month contract for May 2020 closes at -$37.63 per FRED DCOILWTICO: for the first time in history, long position holders arriving at expiration must pay to discharge their obligation of physical receipt at Cushing. Three factors add up. First, global demand collapses by more than 25 Mb/d in April 2020 (per EIA), due to lockdown and near-total halt of air transport. Second, OPEC+ and Russia fail to agree on a coordinated cut in early March 2020; Saudi Arabia even temporarily increases its production. Third, Cushing storage saturates, making physical receipt impossible for long holders arriving at expiration. A closer look: the disinflationary switch of 2020.

The episode is rich in methodological lessons. The negative price of -$37.63 is a physical contract anomaly, not a signal on the fundamental value of crude as a commodity. The Brent series (FRED DCOILBRENTEU), which operates on cash settlement, never touched negative prices despite the same context of collapsed demand. This episode empirically confirms the role of settlement mechanics in the formation of the observed price. More on this: our mapping of oil, gas and metals markets.

The seventh shock is the Russian invasion of Ukraine in March 2022. On March 8, 2022, WTI peaks at $123.70 per FRED (post-2008 peak). The shock combines supply (G7 sanctions on Russian crude, rapid European repositioning), geopolitics (broadening uncertainty over European energy security), and financial stress (flight to commodities as inflation hedge). But the magnitude remains below the 2008 peak ($145), for two reasons. On one hand, U.S. shale offers a marginal adjustment capacity that traditional OPEC+ did not provide in 2008. On the other hand, the G7 price cap mechanism on Russian crude (instituted December 2022 at $60 on Urals) limits the effective withdrawal of Russian supply, which continues to flow to India, China, and Turkey at the capped price.

WTI’s return to the $70-85 corridor since late 2023 illustrates the joint stabilizing effect of shale as swing producer, the structural slowdown of Chinese demand, and OPEC+ discipline. The post-2020 sequence is thus characterized by higher global volatility than the 2010-2020 decade, but with an upper bound moderated relative to historical peaks. Background: Eco3min’s commodity price data, which situates these episodes against the broader complex.

For the empirical audit of the oil burden specific to each of the recessions that followed these shocks, Eco3min has published a dedicated study with case-by-case datavisualizations. Beyond the cluster, the tracking of WTI shocks fits within the broader panorama of commodity cycles in the global economy and within energy geoeconomics which structures the reading of physical markets at Eco3min.

- Seven major shocks since 1973: Arab embargo (1973), Iranian Revolution (1979), Gulf War (1990), China super-cycle (2003-2008), Arab Spring (2011), COVID shock (April 2020, negative price -$37.63), Russian invasion of Ukraine (March 2022, peak $123.70)

- Three combinatorial ingredients identify the nature of the shock: physical supply constraint, structural demand pull, financial stress — each shock combines the three in variable doses

- The supply shocks of the twentieth century (1973, 1979, 1990) preceded U.S. recessions; the 2003-2008 super-cycle and Ukraine 2022 also corresponded to oil burdens above the 4% critical threshold

- The 2020 COVID episode illustrates the physical settlement mechanics of the NYMEX contract: -$37.63 is a contract anomaly, not a fundamental signal on the value of crude

Last updated — 12 July 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

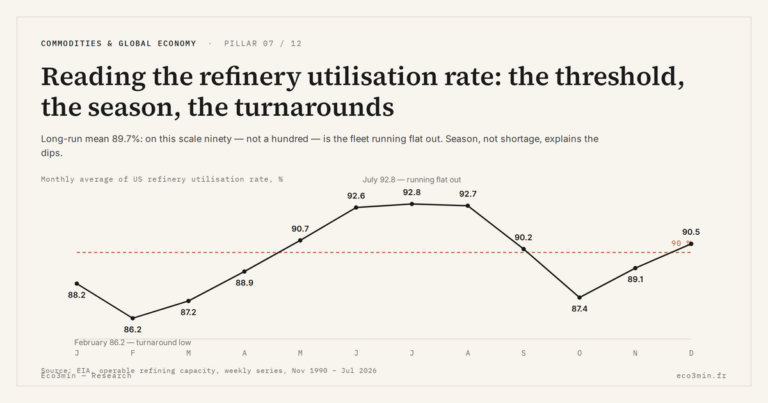

Full pillar →Reading the refinery utilisation rate: the threshold, the season, the turnarounds

A refinery runs full near ninety percent, not a hundred: the last slice of nameplate capacity is a…

IMO 2020: the regulatory shock that rewrote product spreads

An environmental rule on marine sulfur can move a refining spread more than a swing in crude. IMO…

The 2022–2023 refining golden age: anatomy of an episode

In 2022, refined fuel prices climbed faster than crude. That gap, measured by the 3-2-1 crack spread, reached…